Asset managers’ expectations about the economy are all over the place, but most aren’t predicting the worst. The bond market, however, expects the Federal Reserve to cut its federal funds rate in the short term, which it usually does to avoid the risk of recession. In late February 2024, bond futures prices suggested that the Fed would cut its key federal funds rate to 4.5% by the end of 2024, from 5.5% at the time.

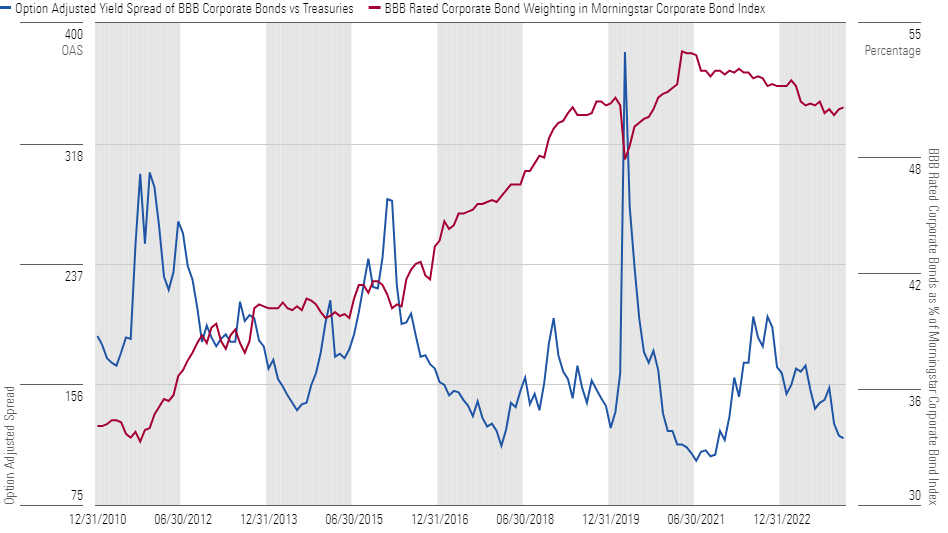

There is, however, a long-term shift in part of the bond market that could prove even more sensitive if we find ourselves in a recession. Although corporate bonds are broadly close to their long-term average weighting in the Morningstar US Core Bond Index, the concentration in the sector’s BBB-rated debt (the lowest rung of the credit quality scale investment) of 51% was close to its all-time high. at the end of January 2024. At the same time, the additional yield generated by this market segment relative to U.S. Treasuries has been lower only a few times over the past decade. In other words, the index has been more heavily exposed to lower quality corporate bonds, at a time when these bonds are historically close to their more expensive ones, and therefore are at greater risk of losing money if their returns simply approach the average.

It is extremely difficult to predict when a particular slice of the corporate bond market will underperform. And it’s possible that BBB valuations will remain elevated for some time, especially if the Fed can achieve the elusive goal of a soft landing for the economy. However, falling into a recession would likely be detrimental to the lower, economically sensitive categories of the investment-grade corporate bond universe, such as BBB-rated issues. This is not a doomsday prediction – especially since the problems, in this case, could result in Treasuries underperforming at a time when overall yields continue to fall – but rather ‘a caution that allocations to these bonds may lag further than they might have during previous periods of crisis. economic weakness.

BBB Heavy Funds

In this context, we looked at funds with the most exposure to BBB-rated debt in the Morningstar FundInvestor 500 Index, which are also heavily invested in corporate bonds.

There is a little good news in that many of these offerings performed in a range close to their Morningstar category averages during the 2020 coronavirus sell-off, the most recent severe test of their mettle. Among the largest funds that performed well relative to their categories was Vanguard Intermediate-Term Investment Grade. VFIDX, Vanguard Global Wellesley Income VGYAX and BlackRock Systematic Multi-Strategy BAMBX.

Of course, this is no guarantee that they will perform similarly in a future crisis, but the results of such comparisons are generally indicative of a fund’s temperament.

In contrast, a handful of other Morningstar FundInvestor 500 funds heavily weighted in BBB-rated debt have underperformed their category averages during the coronavirus selloff, including the Vanguard Long-Term Corporate Bond Index. VLTCX, Loomis Sayles Investment Grade Bonds LIGRX and Loomis Sayles Strategic Income NEFZX.

None of this is intended as advice for dumping your funds if they have large BBB concentrations. If one or more funds make up a significant portion of your portfolio, or if a handful of funds do, it would be worth checking whether you have a large collective exposure to these issues. If so, ask yourself if you have as much diversification as you would like.

This article was first published in the February 2024 issue of Investor in the Morningstar Fund. Download a free copy of FundInvestor by visit this website.

Asset managers’ expectations about the economy are all over the place, but most aren’t predicting the worst. The bond market, however, expects the Federal Reserve to cut its federal funds rate in the short term, which it usually does to avoid the risk of recession. In late February 2024, bond futures prices suggested that the Fed would cut its key federal funds rate to 4.5% by the end of 2024, from 5.5% at the time.

There is, however, a long-term shift in part of the bond market that could prove even more sensitive if we find ourselves in a recession. Although corporate bonds are broadly close to their long-term average weighting in the Morningstar US Core Bond Index, the concentration in the sector’s BBB-rated debt (the lowest rung of the credit quality scale investment) of 51% was close to its all-time high. at the end of January 2024. At the same time, the additional yield generated by this market segment relative to U.S. Treasuries has been lower only a few times over the past decade. In other words, the index has been more heavily exposed to lower quality corporate bonds, at a time when these bonds are historically close to their more expensive ones, and therefore are at greater risk of losing money if their returns simply approach the average.

It is extremely difficult to predict when a particular slice of the corporate bond market will underperform. And it’s possible that BBB valuations will remain elevated for some time, especially if the Fed can achieve the elusive goal of a soft landing for the economy. However, falling into a recession would likely be detrimental to the lower, economically sensitive categories of the investment-grade corporate bond universe, such as BBB-rated issues. This is not a doomsday prediction – especially since the problems, in this case, could result in Treasuries underperforming at a time when overall yields continue to fall – but rather ‘a caution that allocations to these bonds may lag further than they might have during previous periods of crisis. economic weakness.

BBB Heavy Funds

In this context, we looked at funds with the most exposure to BBB-rated debt in the Morningstar FundInvestor 500 Index, which are also heavily invested in corporate bonds.

There is a little good news in that many of these offerings performed in a range close to their Morningstar category averages during the 2020 coronavirus sell-off, the most recent severe test of their mettle. Among the largest funds that performed well relative to their categories was Vanguard Intermediate-Term Investment Grade. VFIDX, Vanguard Global Wellesley Income VGYAX and BlackRock Systematic Multi-Strategy BAMBX.

Of course, this is no guarantee that they will perform similarly in a future crisis, but the results of such comparisons are generally indicative of a fund’s temperament.

In contrast, a handful of other Morningstar FundInvestor 500 funds heavily weighted in BBB-rated debt have underperformed their category averages during the coronavirus selloff, including the Vanguard Long-Term Corporate Bond Index. VLTCX, Loomis Sayles Investment Grade Bonds LIGRX and Loomis Sayles Strategic Income NEFZX.

None of this is intended as advice for dumping your funds if they have large BBB concentrations. If one or more funds make up a significant portion of your portfolio, or if a handful of funds do, it would be worth checking whether you have a large collective exposure to these issues. If so, ask yourself if you have as much diversification as you would like.

This article was first published in the February 2024 issue of Investor in the Morningstar Fund. Download a free copy of FundInvestor by visit this website.