Key takeaways

- Investors will be better served by longer duration bonds.

- Long-term interest rates are expected to fall further.

- The Federal Reserve will begin cutting rates, perhaps as early as March.

- Corporate credit spreads provide an adequate margin of safety against downgrade and default risk.

The bond market rebounds in 2023

After experiencing the worst bond market on record in 2022, bond markets have largely normalized and rebounded in 2023. Year-to-date, fixed income yields have been positive, with bonds trading at a credit spread having performed better than US Treasuries.

Through December 5, the Morningstar US Core Bond Index, our indicator of the broader bond market, was up 2.77%. Return was supported by a combination of underlying yield carry and tightening credit spreads, slightly offset by a rise in long-term interest rates.

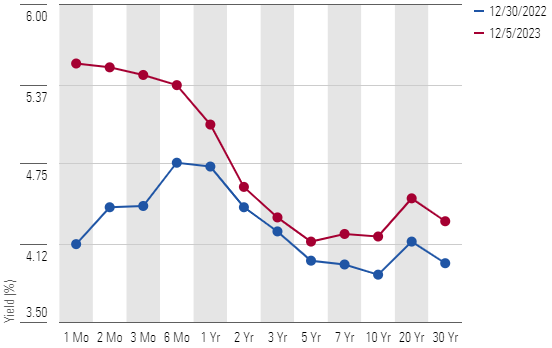

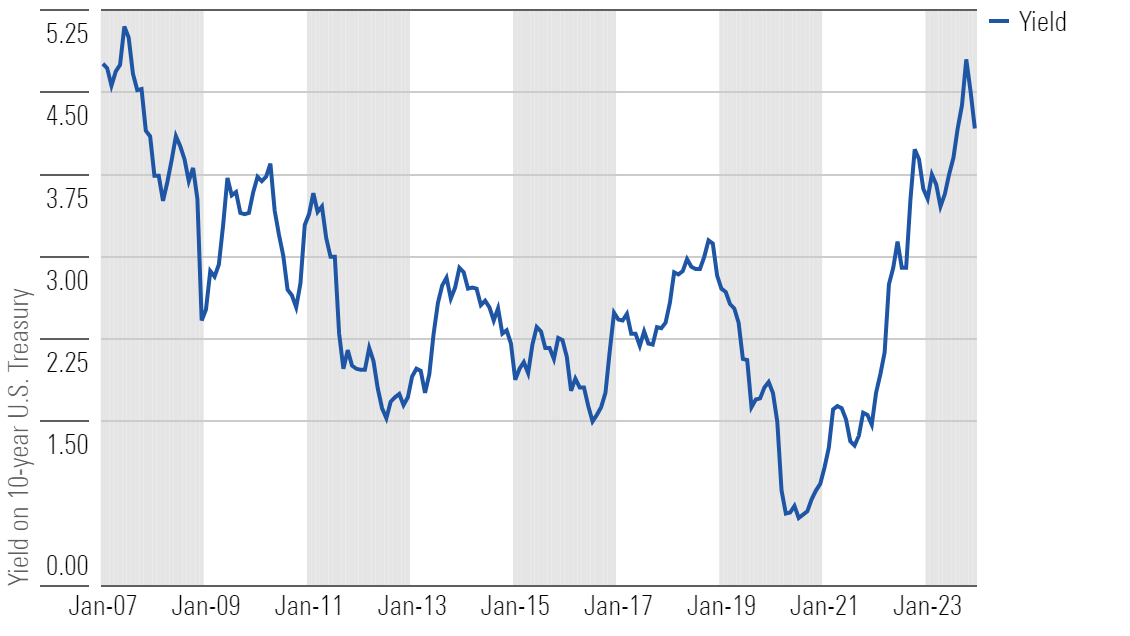

Throughout 2023, the yield curve has further inverted. Short-term interest rates rose as the Federal Reserve raised the federal funds rate, reaching a range of 5.25% to 5.50% after starting the year in a range of 4.25%. at 4.50%. High inflation, quantitative tightening and other technical factors pushed the yield on the 10-year U.S. Treasury to 4.18%, an increase of 30 basis points from the start of the year.

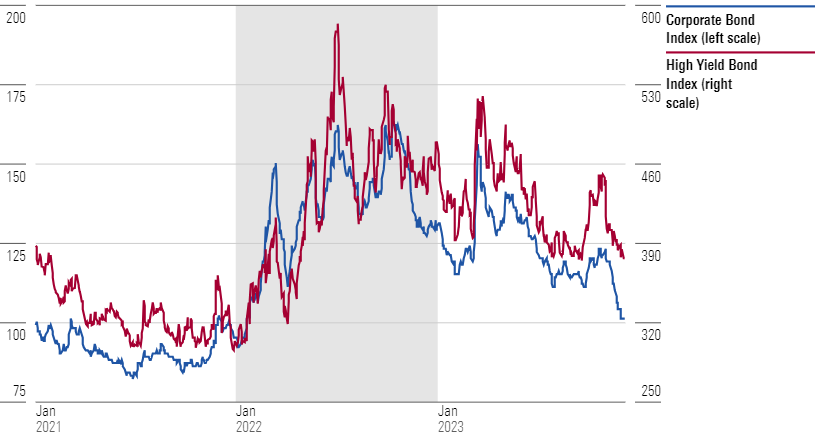

Bonds that trade with an additional credit spread over equivalent-maturity U.S. Treasury bonds have performed the best so far this year. For example, the Morningstar U.S. Corporate Bond Index (our indicator of investment-grade corporate bonds) increased 5.49% and the Morningstar U.S. High Yield Bond Index increased 10.14%. . The reason for this outperformance was twofold. First, these bonds offer a higher yield to compensate investors against the risk of credit rating downgrade or default. Second, credit spreads tightened over the year.

Through Dec. 5, the average corporate credit spread in the Morningstar U.S. Corporate Bond Index tightened 29 basis points to plus-101. The average corporate credit spread in the Morningstar U.S. High Yield Bond Index tightened 103 basis points to plus-376.

Bond investment outlook in 2024

After starting the year recommending investors focus on the middle of the yield curve, we began advising investors to lengthen their duration in our Mid-Year Bond Market Update. Our forecast is that we continue to believe that investors will be better served by longer duration bonds and maintaining current high interest rates.

In the near term, we expect the Fed to change course and begin easing monetary policy in 2024 by lowering the federal funds rate. This forecast is based on the combination of our projections that inflation will continue to moderate and the rate of economic growth will slow.

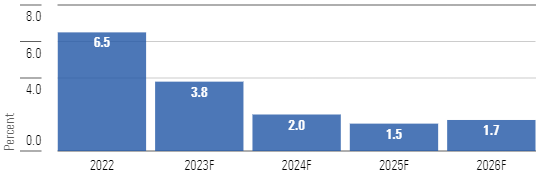

From pandemic-induced shifts in consumption patterns to supply chain disruptions to geopolitical events, inflation rose more than expected in 2022. Inflation has declined steadily in 2023, and we expect to may this trend continue. Looking ahead, the conditions that spurred inflation have largely normalized. We expect deflationary forces in these specific categories to significantly slow the overall inflation rate.

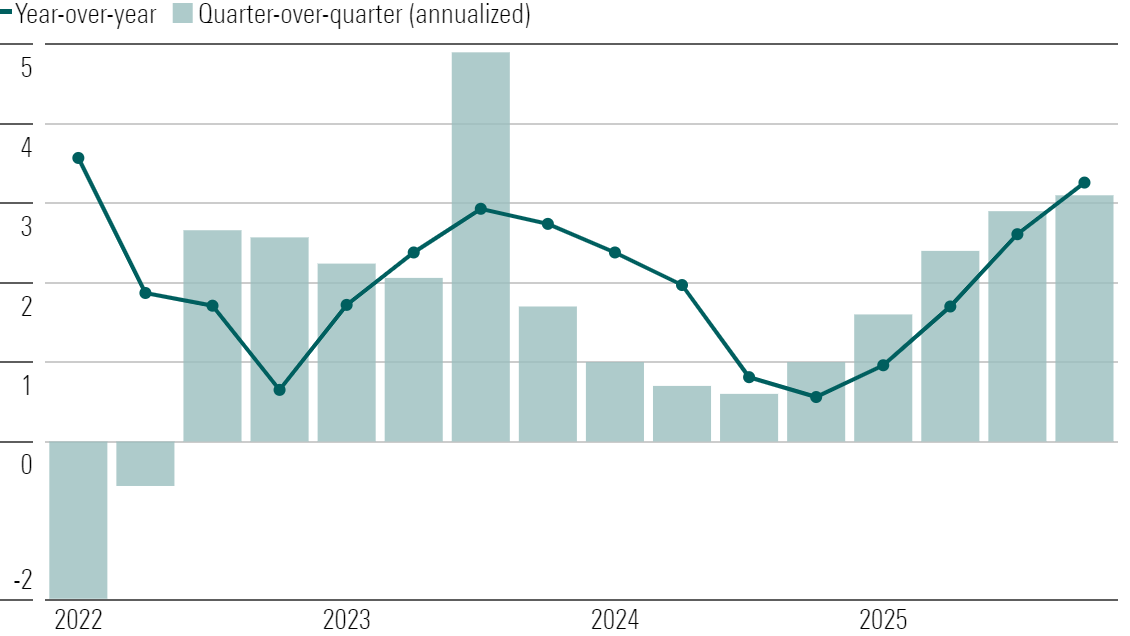

Restrictive monetary policy and current high interest rates will have adverse consequences on the economy. Although our base case remains that there will be no recession, we expect the rate of economic growth to slow. We forecast that real gross domestic product will decelerate at an annualized rate of 1.7% in the fourth quarter of 2023 and will continue to slow sequentially each quarter until reaching its low point in the third quarter of 2024. We then forecast that the rate of economic growth will increase throughout the period. 2025.

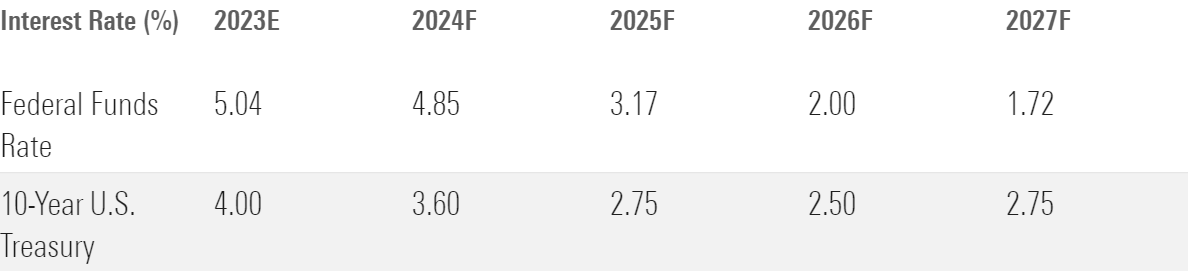

We expect the Fed to lower the federal funds rate at its March 2024 meeting and continue its decline to around 3.75% by the end of the year. We further expect the Fed to continue cutting rates, bringing them down to 2.25% by the end of 2025. Although short-term rates are currently high, they will decline relative to the federal funds rate and to as short-term debt matures. , investors will have the opportunity to reinvest at lower rates.

At the longer end of the curve, we expect the 10-year U.S. Treasury yield to decline and average 3.60% in 2024. We expect the yield to decline further in 2025 and average 3.60% in 2024. will average 2.75%. As interest rates fall, investors will not only benefit from currently high interest rates, but will also benefit from additional price appreciation of longer-dated bonds.

Corporate bond market outlook for 2024

In our 2023 bond market outlook, we noted that we saw value in the wide credit spreads offered by corporate bonds. Since then, corporate credit spreads have tightened and are now within a range that we consider fairly valued.

During the first half of 2024, credit spreads may come under pressure as the economy weakens, and the market may price in the expectation of further downgrades and defaults. Although our base case scenario calls for slowing economic growth in the first three quarters of the year, we do not expect the U.S. economy to fall into recession. We therefore believe that downgrades and defaults will remain close to historically normalized levels. According to PitchBook, the default rate in the leveraged loan market was 1.48% as of November 2023, compared to the 10-year average of 1.58%.

Although the amount of additional spreads granted to corporate bonds seems adequate given our economic outlook, credit spreads are by no means cheap. Over the past 23 years, the Morningstar U.S. Corporate Bond Index spread has been lower than the current spread of plus-101 basis points only 18% of the time. Over the same period, only 25% of the time has the spread of the Morningstar US High Yield Bond Index been lower than its current spread of plus-376 basis points.

Key takeaways

- Investors will be better served by longer duration bonds.

- Long-term interest rates are expected to fall further.

- The Federal Reserve will begin cutting rates, perhaps as early as March.

- Corporate credit spreads provide an adequate margin of safety against downgrade and default risk.

The bond market rebounds in 2023

After experiencing the worst bond market on record in 2022, bond markets have largely normalized and rebounded in 2023. Year-to-date, fixed income yields have been positive, with bonds trading at a credit spread having performed better than US Treasuries.

Through December 5, the Morningstar US Core Bond Index, our indicator of the broader bond market, was up 2.77%. Return was supported by a combination of underlying yield carry and tightening credit spreads, slightly offset by a rise in long-term interest rates.

Throughout 2023, the yield curve has further inverted. Short-term interest rates rose as the Federal Reserve raised the federal funds rate, reaching a range of 5.25% to 5.50% after starting the year in a range of 4.25%. at 4.50%. High inflation, quantitative tightening and other technical factors pushed the yield on the 10-year U.S. Treasury to 4.18%, an increase of 30 basis points from the start of the year.

Bonds that trade with an additional credit spread over equivalent-maturity U.S. Treasury bonds have performed the best so far this year. For example, the Morningstar U.S. Corporate Bond Index (our indicator of investment-grade corporate bonds) increased 5.49% and the Morningstar U.S. High Yield Bond Index increased 10.14%. . The reason for this outperformance was twofold. First, these bonds offer a higher yield to compensate investors against the risk of credit rating downgrade or default. Second, credit spreads tightened over the year.

Through Dec. 5, the average corporate credit spread in the Morningstar U.S. Corporate Bond Index tightened 29 basis points to plus-101. The average corporate credit spread in the Morningstar U.S. High Yield Bond Index tightened 103 basis points to plus-376.

Bond investment outlook in 2024

After starting the year recommending investors focus on the middle of the yield curve, we began advising investors to lengthen their duration in our Mid-Year Bond Market Update. Our forecast is that we continue to believe that investors will be better served by longer duration bonds and maintaining current high interest rates.

In the near term, we expect the Fed to change course and begin easing monetary policy in 2024 by lowering the federal funds rate. This forecast is based on the combination of our projections that inflation will continue to moderate and the rate of economic growth will slow.

From pandemic-induced shifts in consumption patterns to supply chain disruptions to geopolitical events, inflation rose more than expected in 2022. Inflation has declined steadily in 2023, and we expect to may this trend continue. Looking ahead, the conditions that spurred inflation have largely normalized. We expect deflationary forces in these specific categories to significantly slow the overall inflation rate.

Restrictive monetary policy and current high interest rates will have adverse consequences on the economy. Although our base case remains that there will be no recession, we expect the rate of economic growth to slow. We forecast that real gross domestic product will decelerate at an annualized rate of 1.7% in the fourth quarter of 2023 and will continue to slow sequentially each quarter until reaching its low point in the third quarter of 2024. We then forecast that the rate of economic growth will increase throughout the period. 2025.

We expect the Fed to lower the federal funds rate at its March 2024 meeting and continue its decline to around 3.75% by the end of the year. We further expect the Fed to continue cutting rates, bringing them down to 2.25% by the end of 2025. Although short-term rates are currently high, they will decline relative to the federal funds rate and to as short-term debt matures. , investors will have the opportunity to reinvest at lower rates.

At the longer end of the curve, we expect the 10-year U.S. Treasury yield to decline and average 3.60% in 2024. We expect the yield to decline further in 2025 and average 3.60% in 2024. will average 2.75%. As interest rates fall, investors will not only benefit from currently high interest rates, but will also benefit from additional price appreciation of longer-dated bonds.

Corporate bond market outlook for 2024

In our 2023 bond market outlook, we noted that we saw value in the wide credit spreads offered by corporate bonds. Since then, corporate credit spreads have tightened and are now within a range that we consider fairly valued.

During the first half of 2024, credit spreads may come under pressure as the economy weakens, and the market may price in the expectation of further downgrades and defaults. Although our base case scenario calls for slowing economic growth in the first three quarters of the year, we do not expect the U.S. economy to fall into recession. We therefore believe that downgrades and defaults will remain close to historically normalized levels. According to PitchBook, the default rate in the leveraged loan market was 1.48% as of November 2023, compared to the 10-year average of 1.58%.

Although the amount of additional spreads granted to corporate bonds seems adequate given our economic outlook, credit spreads are by no means cheap. Over the past 23 years, the Morningstar U.S. Corporate Bond Index spread has been lower than the current spread of plus-101 basis points only 18% of the time. Over the same period, only 25% of the time has the spread of the Morningstar US High Yield Bond Index been lower than its current spread of plus-376 basis points.