The private credit market, in which specialized non-bank financial institutions such as investment funds lend to businesses, exceeded $2.1 trillion in assets and committed capital last year. About three-quarters of this was made in the United States, where its market share approaches that of syndicated loans and high-yield bonds.

This market emerged about thirty years ago as a source of financing for companies too large or too risky for commercial banks and too small to raise debt on public markets. Over the past few years, it has grown rapidly as features such as speed, flexibility and attentiveness have proven valuable to borrowers. Institutional investors such as pension funds and insurance companies enthusiastically invested in funds which, although illiquid, offered higher returns and less volatility.

Private business credit has generated significant economic benefits by providing long-term financing to corporate borrowers. However, the migration of these loans from regulated banks and more transparent public markets to the more opaque world of private credit creates potential risks. Valuations are rare, credit quality is not always clear or easy to assess, and it is difficult to understand how systemic risks can develop given the unclear interconnections between private credit funds, capital firms -investment, commercial banks and investors.

Today, the immediate risks linked to private credit for financial stability appear limited. However, given that this ecosystem is opaque and highly interconnected, and if rapid growth continues with limited oversight, existing vulnerabilities could become a systemic risk to the financial system as a whole.

We identify a number of fragilities in our April 2024 Global Financial Stability Report.

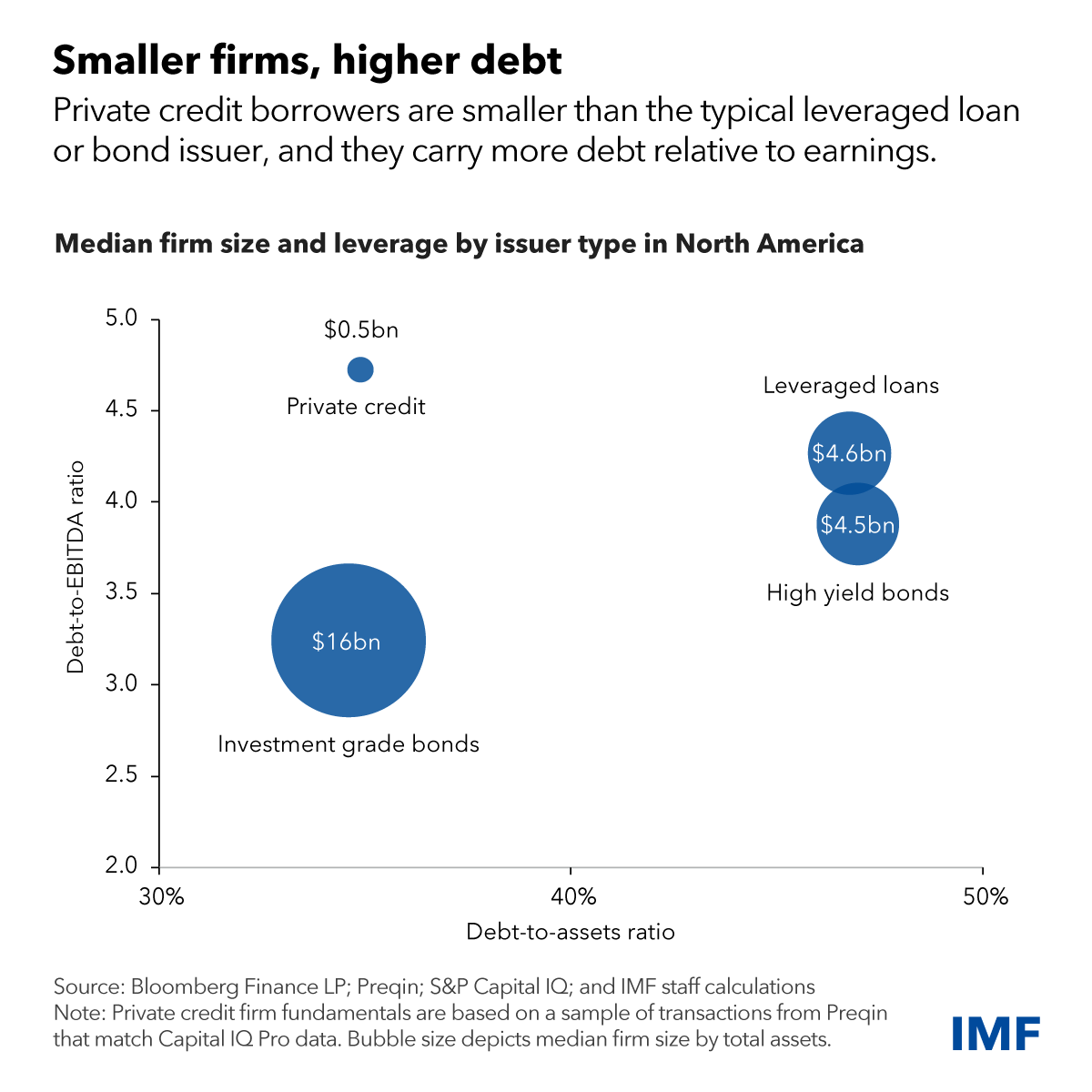

First, firms using the private credit market tend to be smaller and more leveraged than their counterparts using leveraged loans or public bonds. This makes them more vulnerable to rising rates and economic downturns. With the recent rise in benchmark interest rates, our analysis indicates that more than a third of borrowers now have interest costs higher than their current income.

The rapid growth of private credit has recently led to increased competition from banks for large transactions. This in turn has put pressure on private credit providers to deploy capital, leading to lower underwriting standards and looser loan terms, some signs of which have already been noted by the supervisory authorities.

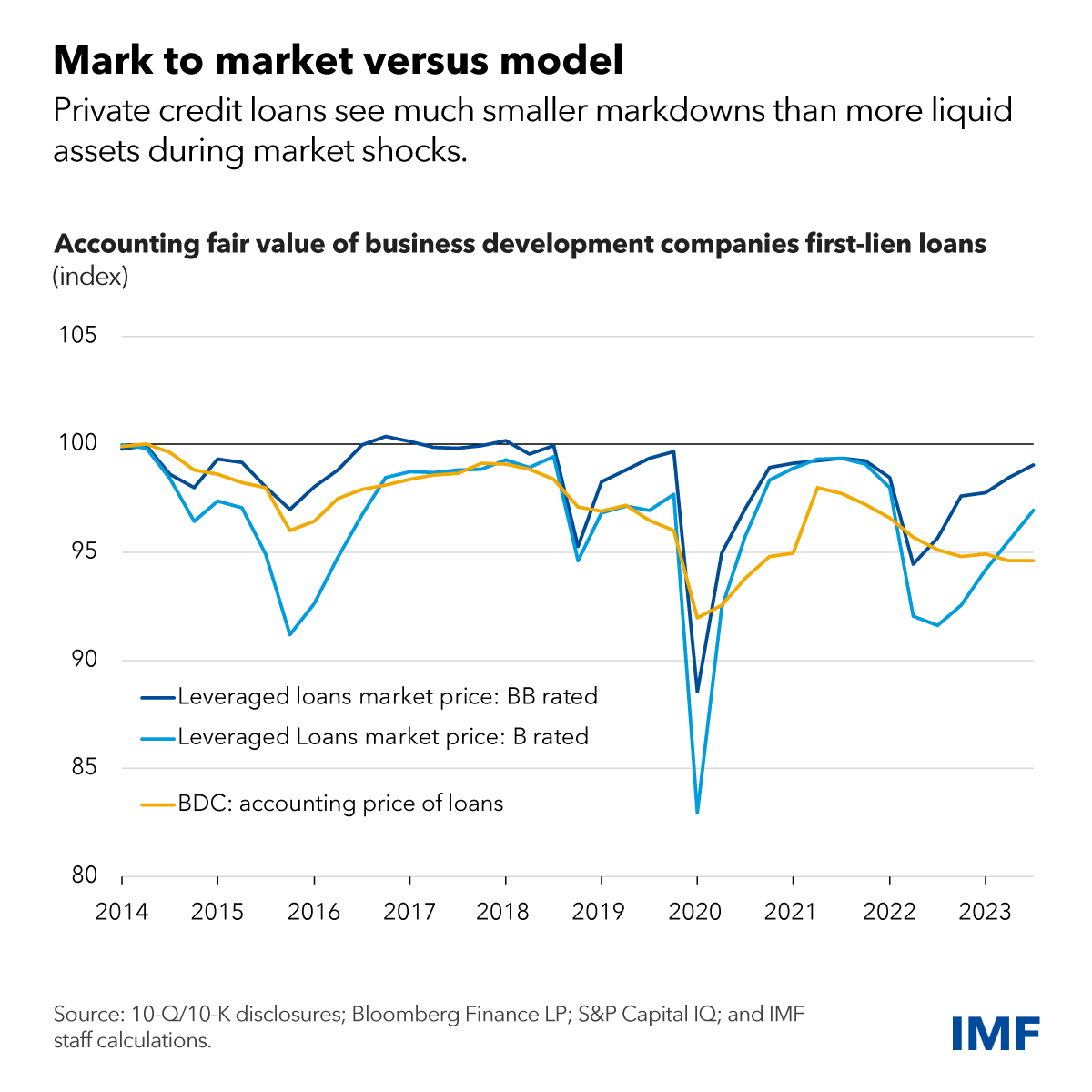

Second, private market loans are rarely traded and therefore cannot be valued using market prices. Instead, they are often only valued quarterly using risk models and can suffer from outdated and subjective valuations between funds. Our analysis comparing private credit to leveraged loans (which regularly trade in a more liquid and transparent market) shows that, despite lower credit quality, private credit assets tend to experience lower markdowns in periods tensions.

Third, although the leverage of private credit funds appears low, the possibility of multiple levels of hidden leverage within the private credit ecosystem raises concerns given the lack of data. Leverage is also deployed by investors in these funds and by the borrowers themselves. This stratification of leverage makes it difficult to assess the potential systemic vulnerabilities of this market.

Fourth, there appears to be a significant degree of interdependence within the private credit ecosystem. Although banks do not appear to have significant exposure to private credit overall – the Federal Reserve has estimated that private credit borrowing in the United States is less than about $200 billion, or less than 1% of U.S. bank assets. – some banks may have concentrated their private credit exposures overall. The area. Additionally, a select group of pension funds and insurers are wading deeper into the private credit waters, significantly increasing their share of these less liquid assets. This includes private equity-influenced life insurance companies, as we discussed in a recent report.

Finally, even if liquidity risks seem limited today, a growing presence of retailers could modify this assessment. Private credit funds use long-term capital locks and impose constraints on investor redemptions to align the investment horizon with the underlying illiquid assets. But new funds aimed at individual investors may have higher redemption risks. Although these risks are mitigated by liquidity management tools (such as gates and fixed redemption periods), they have not been tested in a severe liquidation scenario.

Overall, although these vulnerabilities do not currently pose a systemic risk to the financial sector as a whole, they could continue to become more pronounced, with implications for the economy. In the event of a severe recession, credit quality could deteriorate significantly, causing defaults and significant losses. Opacity could make these losses difficult to assess. Banks could restrict lending to private credit funds, retail funds could face significant redemptions, and private credit funds and their institutional investors could experience liquidity stress. Significant interconnectivity could affect public markets, as insurance companies and pension funds could be forced to sell more liquid assets.

The cumulative effect of these links could have significant economic implications if strains in private credit markets lead to a withdrawal of lending to businesses. Serious data gaps make it more difficult to monitor these vulnerabilities in financial markets and institutions and can delay appropriate risk assessment by policymakers and investors.

Political implications

It is imperative to adopt a more vigilant regulatory and supervisory posture to monitor and assess risks in this market.

-

Authorities should consider a more active approach to supervision and regulation of private credit, focusing on monitoring and risk management, leverage, interconnectivity and concentration of exposures.

-

Authorities should strengthen cooperation across industry sectors and national borders to close data gaps and make risk assessments more consistent across financial sectors.

-

Regulators should improve reporting standards and data collection to better monitor private credit growth and its implications for financial stability.

-

Securities regulators should pay particular attention to liquidity and conduct risk in private credit funds, particularly retail, which may face higher redemption risks. Regulators should implement recommendations from the Financial Stability Board and the International Organization of Securities Commissions on product design and liquidity management.

—This blog is based on Chapter 2 of the April 2024 Global Financial Stability Report: “The Rise and Risks of Private Credit.”