NanoStockk

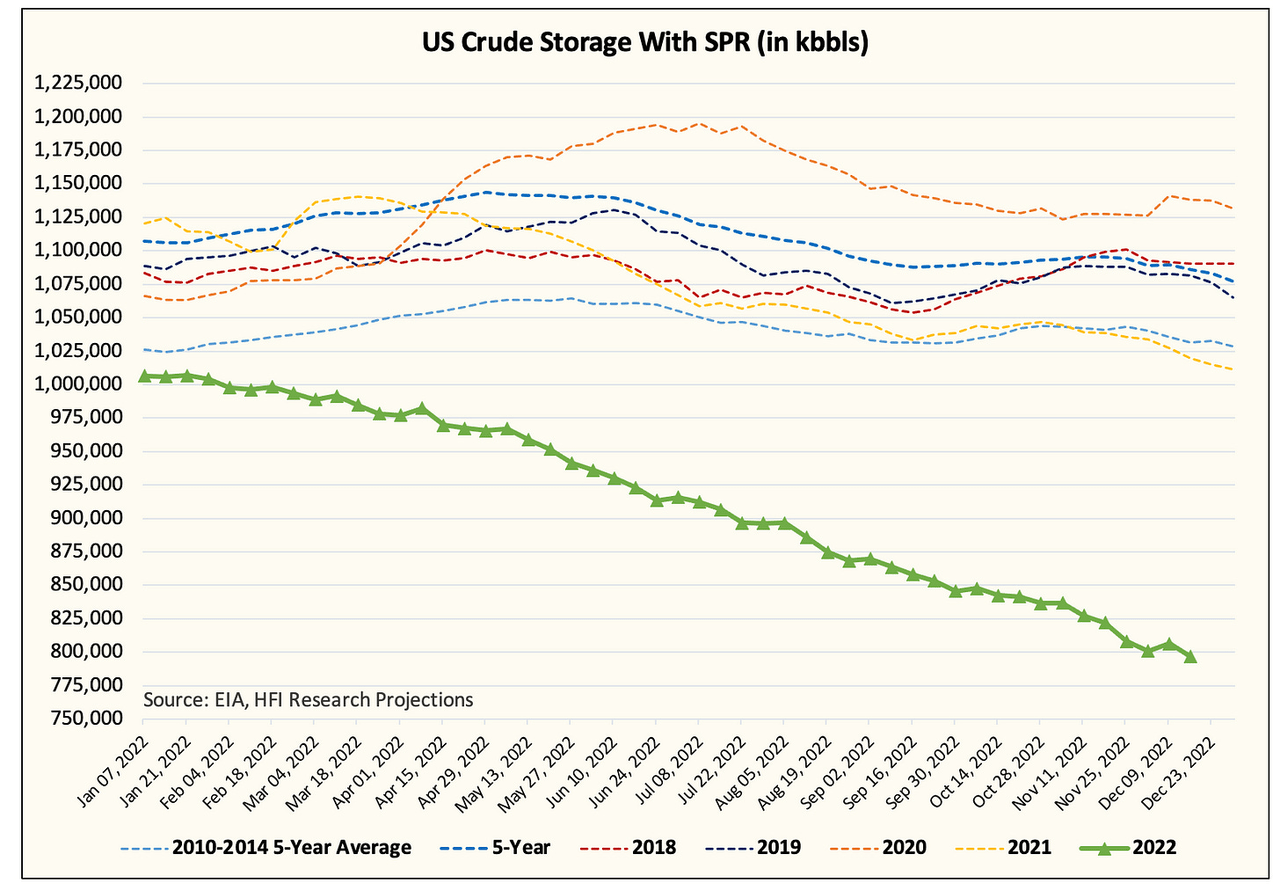

The EIA reported a “bearish” report today. But we suspect traders can easily see through this data. In our weekly U.S. Crude Storage Outlook Report, we informed our subscribers that this week’s crude figure will be heavily impacted by a significant drop in U.S. crude exports. This figure is expected to reverse next week, pushing US crude storage lower again.

Our preliminary estimate indicates that US crude with SPR is expected to fall below around 800 million barrels in next week’s report.

EIA, HFIR

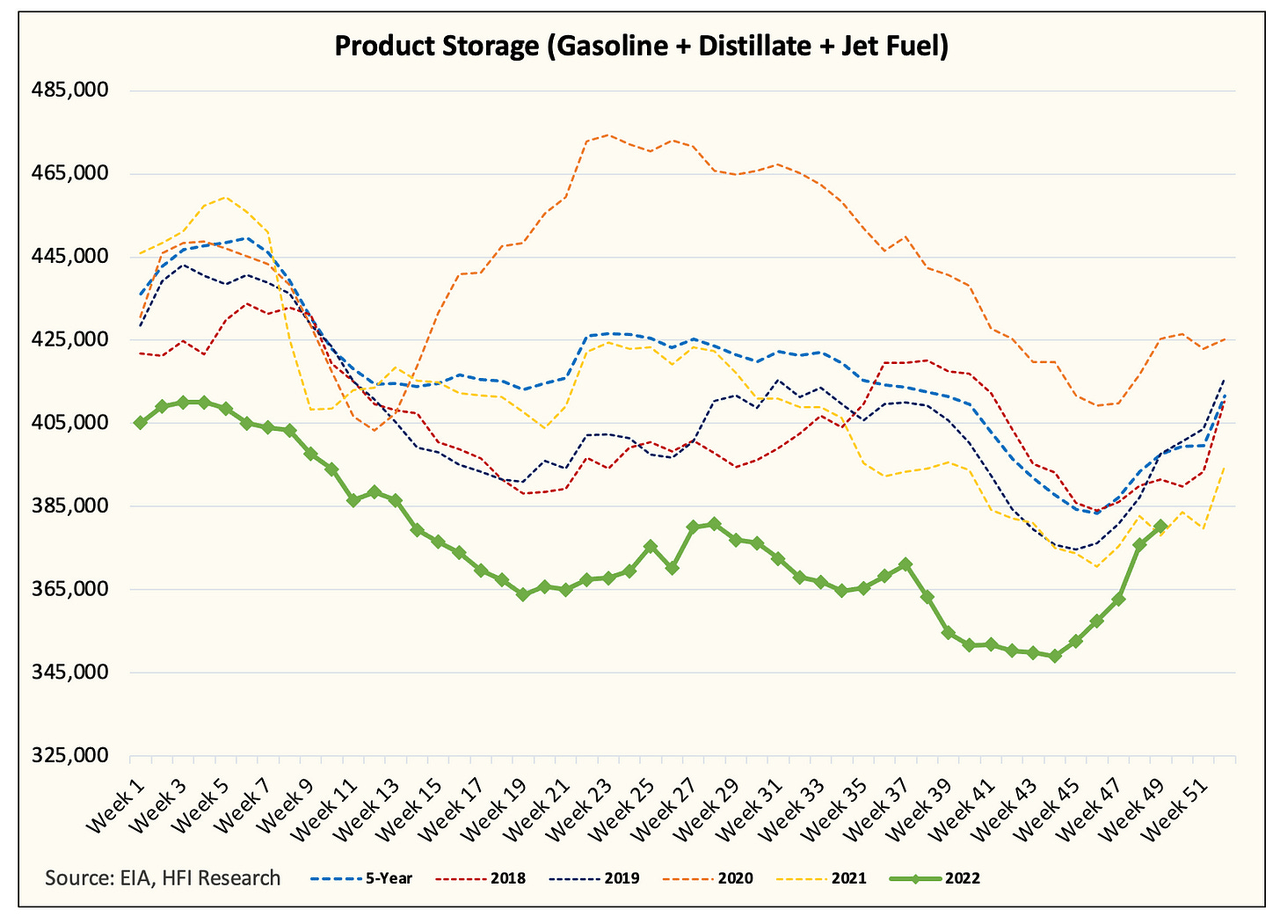

As for product storage, we build seasonally until the end of the year for tax purposes. While the pace of construction has accelerated, total product inventory is still tight compared to historical averages.

EIA, HFIR

Essentially, we think the market is ignoring this one-time bearish report. With US crude exports expected to remain elevated through the end of the year, readers should expect crude storage to continue to accumulate, while commodity storage should continue to expand.

Most important for the oil market is China’s return to the physical oil market scene. Looking at the Brent time spreads, we are starting to see the contango disappear.

Barchart.com

And like Oil Bandit reported on Twitter, Unipec has just recovered 5 VLCCs. The reopening of China is far more important to the balance of the oil market than any other variable. The reopening also comes at a time when Russian crude exports are finally starting to decline.

As we detailed in our two reports this week on how the oil speculators are fucking the pooch, we think the timing of everything is just too perfect.

And after?

The oil market will need to see continued demand from China and the current decline in Russian crude exports materialize. If so, the backwardation should return, which should signal to the market that the first quarter balances are not as bad as expected. We should also see crack spreads improve in the future, which would indicate that end-user demand is doing well.

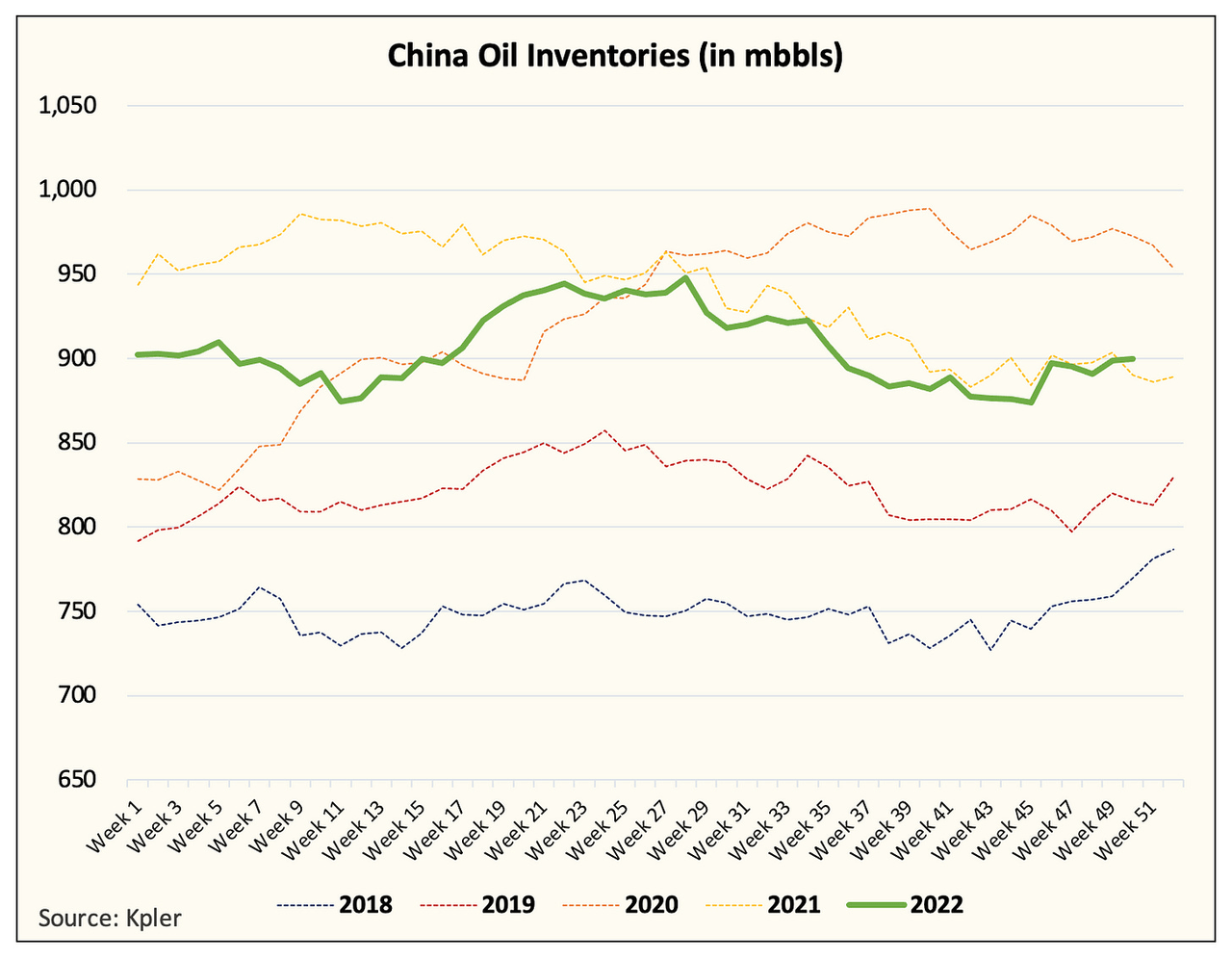

A caveat in all of this will be the pace of China’s return to the oil market. Given the current oil price situation (below $95 Brent), we believe China is more likely to buy crude on the open market than use what is stored. But as oil begins to rise again, China will use its vast crude inventories to “control” prices. Similar to what the US did this year with SPR, we suspect China will do the same later.

kpler

Given all the COVID restrictions lifted in China, demand for oil is expected to surprise on the upside, which would drastically reduce its product surplus in a rapid manner. This will be reflected in the cracks in Singapore first, and when it does, that’s when you’ll know China is back in full force.

Meanwhile, there is a large technical resistance level for WTI around $82-$84. For many dynamic funds, this is the level that WTI must break above before bullish cash flows return. Given the level of short-term interest in WTI and Brent, we think any signs of tightening in the physical market (whether from China or Russia) should drive prices higher.

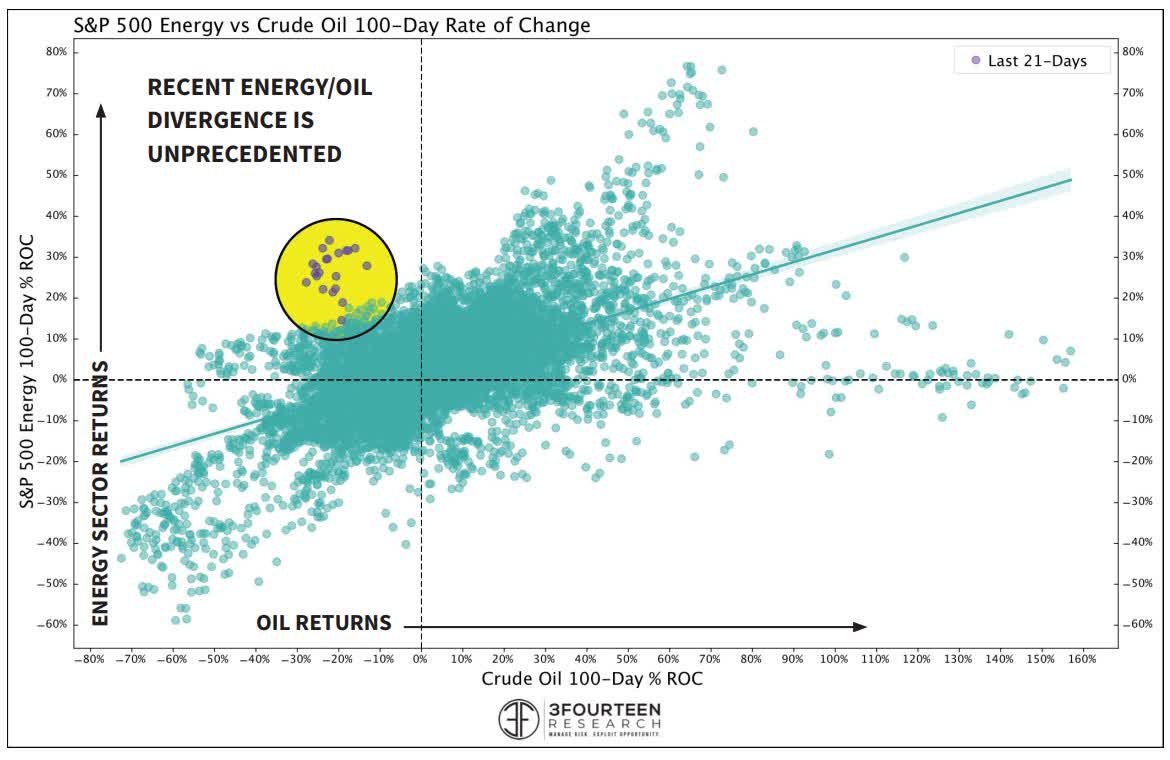

As for energy stocks, they held up much better to the oil selloff than we had expected. Warren pies This relationship is best illustrated in the table below:

Warren pies

Warren noted that this divergence has always been resolved with the rally in oil. We think readers should expect energy stocks to hold steady/slowly trend higher, while oil corrects much of the divergence.

Overall, the physical oil market red flags we noted last week turned out to be a false alarm. With the return of China and the loss of crude exports by Russia, the contango that we see in the market should disappear, allowing the return of backwardation. Once WTI breaks above this resistance level, momentum funds and CTAs should get back into the bullish trade.