Leestat

Vanguard FTSE Europe ETF (NYSEARCA:VGK) gives investors broad exposure to Europe, but there aren’t a whole lot of reasons to want that. While some of the exposures are resilient, all have a good share of wallet in Europe. For US Investors there is the currency problem, but even for European investors there are many reasons to worry about the economic state of Europe as the war in Ukraine continues to rage. The recession is already evident, and financial risks are not benefiting from the more aggressive rate hikes underway in other regions. European rate hikes will never compare to what the US just did, and their economy will continue to languish as they foot the bill for what is effectively a proxy war in Ukraine. Europe loses its influence over the next decade and is not worth your investment.

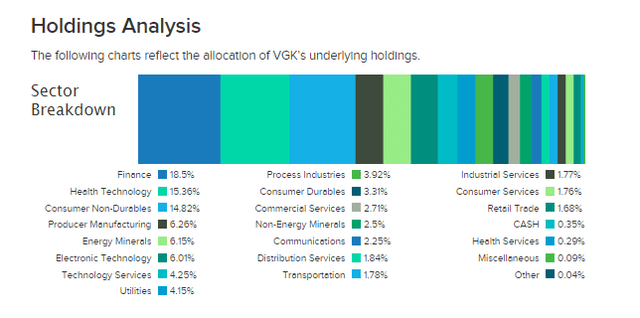

VGK Breakdown

Let’s take a quick look at sector exposures to get started.

Sector exposures (etfdb.com)

In a global economic regime of rising rates, financial exposures, whether insurance or banking, would be favorable as lending rates rise more than deposit rates. The problem is that European inflation is more cost driven than elsewhere due to their previous reliance on Russian gas which no longer flows, and their fairly rapid exit from coal in all but Germany over the past 5 years, as well as nuclear ignorance with the exception of France and to a lesser extent Spain. Outside of Norway there is not much oil either. Britain has never done fracking and oil is far from the focus, with many European refineries turning into renewable diesel operations. Rising rates will not help inflation and the ECB knows it. Rates in Europe are barely above 2% today, and that’s why. There is no great tailwind for European banks and insurance companies.

Health care cannot be faulted here. Exhibitions like Novartis (NVS), Astra Zeneca (AZN) and others may have slight idiosyncratic issues, Roche (OTCQX:RHHBY) also with its COVID diagnostics business, but ultimately whether the European portfolio shares or not, the recession resistance is there. US investors may still be concerned about the overall risk of the euro, but the fundamentals will be quite strong for the most part.

For the rest of the portfolio, while non-durables might do more or less well, the recession in Europe will still affect them, and for manufacturing, industrials and cyclicals, it will get worse and worse. Automotive is not insignificant in the European basin, and it continues to benefit from pent-up demand that could suddenly evaporate into much weaker demand in a high rate environment.

Conclusion

The war in Ukraine has disrupted European energy supplies and forced them into costly alternative arrangements. The beneficiaries of this dislocation are found in East and Southeast Asia. The United States is able to export gas at high prices, and the strength of the dollar due to lower cost pressures and the possibility of larger rate hikes has put their country’s finances and current account in a difficult position. good situation. Reparations for the war in Ukraine have already been started by Europe, so that’s where they are footing the bill. Europe is on the rocks, and their economic strength, even that of Germany which was a beacon in the region, will see a permanent relative decline over the next two years. VGK shares have a large European wallet share, and many industries, especially manufacturing, are beginning to feel pressure in European markets and are in decline. The recession has started and will continue for some time. The loss of influence will continue more secularly as others benefit and consolidate new advantages. Geopolitics really went against them, and for a PE of 17.5x, VGK implies a decent earnings situation despite recessionary pressures and a relatively worse situation in the EU. The multiple is not far from the SPY PE of 20x. No reason to take this bet.

With our global coverage, we have stepped up our global macro commentary on our market service here on Seeking Alpha, The laboratory of value. We focus on long-term value ideas, where we try to find undervalued international stocks and target a portfolio return of around 4%. We’ve done very well over the past 5 years, but we had to get our hands dirty in the international markets. If you are a value-oriented investor concerned with protecting your wealth, we at the Value Lab could be a source of inspiration. Try our no-obligation free trial to see if it’s right for you.