Chancellor of the Exchequer (Finance Minister) Kwasi Kwarteng has granted the biggest tax cut since 1972, amounting to £45 billion, or 1.5% of GDP.

The UK Treasury is to borrow an additional £72bn by April 2023, or around 3% of nominal GDP. These loans are becoming more expensive as central bankers raise interest rates to tame the worst inflation in decades.

The tax cuts, which come on top of a government program to help households and businesses cope with soaring energy prices, ‘will turn the vicious cycle of stagnation into a virtuous cycle of growth’ , Kwarteng said. The government expects that a reduction in the tax burden for businesses and the wealthy will eventually trickle down to higher wages and rising living standards for the rest of the UK.

Investors reacted to the Kwarteng tax cut announcement by hitting the pound and the UK bond market, which could impact interest rates, personal consumption, housing and trade, which faces extensive controls and checks at the former frictionless border with the EU.

Our forecast for the UK is under close scrutiny. We remain cautious about trend growth in the UK, which we continue to recommend around 1.4%. This signals a potential medium-term fiscal drag. If the growth plan fails, the government will have to embrace a prolonged period of tax hikes and spending cuts to restore fiscal discipline.

In search of growth

The proposed income tax and NI cuts will help struggling households and support our assessment that the projected recession is likely to end in early 2023. As additional pressure comes to bear on household budgets, this will probably encourage them to spend more on other goods and services.

We have some reservations. The Chancellor has not asked her independent forecaster, the Office for Budget Responsibility, to produce new growth and borrowing forecasts to accompany the plan, adding to investor concerns. The proposed tax changes will provide only a limited boost to low-income earners, a missed opportunity given their above-average propensity to consume. The freezing of tax thresholds for several years will affect people with average incomes.

A recent Office for National Statistics survey found that UK businesses do not cite tax issues as their top concern, suggesting that tax incentives may struggle to speed up the investment cycle. The latest business surveys suggest that the new rules and regulations that come with the EU-UK Trade and Cooperation Agreement when exporting to the EU will remain a blight on UK businesses in the medium term.

A bumpy road

We expect a bumpy road for UK sovereign borrowing costs and the pound sterling in the coming months.

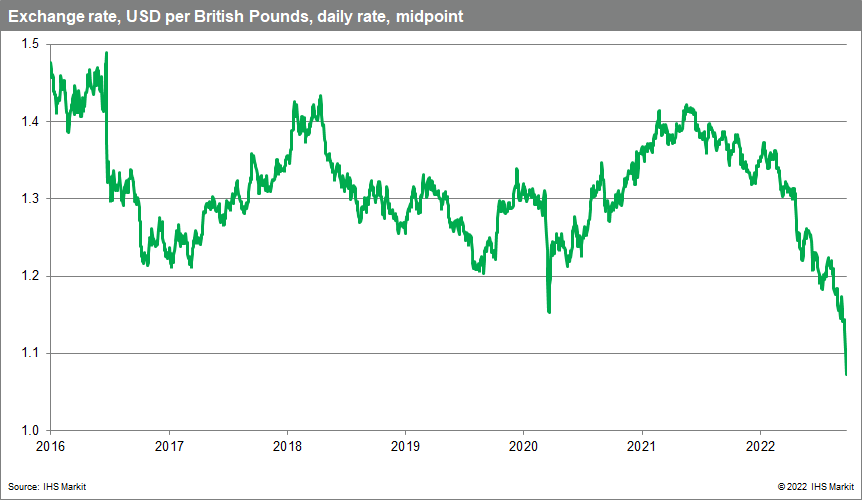

The pound fell to an all-time high of around $1.08. The pound has come under increasing pressure since March as markets grew fearful that runaway inflation could push the UK into recession. Russia’s invasion of Ukraine has triggered a flight to quality, which favors the US dollar, putting further pressure on the pound.

Kwarteng’s announcement also sparked turmoil in the UK bond market. Ten-year borrowing costs hit their highest level since 2011.

The Bank of England (BoE) now faces a bigger task in its own fight against inflation. The central bank may need to send a stronger signal that it is ready to do whatever it takes to bring inflation down. This could include an emergency or an unexpected rate hike.

Central bank pressures

We expect the BoE to stick to its scheduled meetings, especially as it prepares to release new growth and inflation forecasts at its meeting in early November. We also expect a 50 basis point hike in November, followed by 25 basis point hikes at the December 2022, February 2023 and March 2023 meetings, bringing the Bank Rate to a peak of 3.5%.

The BoE is likely under pressure to offer a bigger hike at its scheduled meeting in November, pointing to a higher peak in early 2023.

Given the turbulence in the bond market, the central bank could face challenges to its plan to reduce the stock of UK government bond purchases, financed by the issuance of central bank reserves, £80 billion ($90 billion) over the next 12 months.

Britain’s debt management office will have to step up its efforts to get more issues into the hands of private investors following the tax cut announcement and will have to rely more on foreign investors. The additional borrowing will put pressure on the UK’s current account deficit, which widened to a record £51.7bn, or 8.3% of GDP in the first quarter of 2022.

The inevitable rise in mortgage rates adds to the financial difficulties of British households. Variable rate mortgages account for around one in five of the UK’s 11.1 mortgages. In addition, there are 3.1 million mortgage loan holders whose fixed rate periods expire in 2022-2023.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.