![Fitbit app rolls out sleep stats overhaul to Android and iOS [U] – 9to5Google](https://oltnews.com/wp-content/uploads/2024/04/fitbit-app-sleep-redesign-75x75.jpg)

The securities industry is making significant technological advancements. Where are companies progressing and what is holding them back?

By Monica Summervillehead of capital markets, Celent

As the financial markets of the future emerge, so does the evolution of technology used by the securities industry. The digital transformation of securities firms will largely revolve around developments in three key areas: cloud adoption, mainframe modernization, and how firms leverage data exchange mechanisms.

The Celent Report Preparing for a cloud-based, data-driven world highlights findings from analyst interviews (conducted in 4Q21 and 1Q22) and surveys of 28 technology and operations executives at 19 North American financial institutions (FIs). DTCC, a financial services company that provides clearing and settlement services for capital markets, commissioned Celent to conduct research to provide insight into the industry’s progress on its transformation journey. The analysis of this research illustrates important points for chief information officers (CIOs), chief information security officers (CISOs), chief risk officers (CROs), and line of business leaders ( LOB managers) in financial markets companies on the buy and sell side, as they assess the parallel technology structures needed for a full digital transformation.

- Cloud adoption

The study found that cloud adoption is nearly universal in the securities industry. The main drivers of cloud adoption (for both buyers and sellers) are: increased business agility, increased operational efficiency, and improved security and convenience. resilience. The previous focus on infrastructure as a service (IaaS) and “moving/moving” to the cloud is changing; Businesses are recognizing that realizing the true benefits of the cloud requires fully embracing cloud technologies and new ways of working. Cloud-native and cloud-first approaches (meaning new applications are built as cloud-native) are now prevalent in FIs in the area of securities and investment management.

However, the extent to which an individual FI adopts the cloud varies. Nearly 50% of all study participants can be described as “cloud leaders”. This cohort already has or is moving towards a fully cloud-native stack; their new app development uses cloud-native technologies and modernizing legacy apps is a priority. Most cloud leaders work with multiple public cloud providers, but the study found that AWS and MS Azure together dominate market share in the capital markets industry.

Over the next couple of years, many enterprises will be moving towards large-scale adoption of hybrid private/public cloud. By 2024, about a quarter (28%) of enterprises will be moving to the cloud, deploying some applications in public and private clouds, while maintaining on-premises infrastructure. Keeping IT on-premises is often intended for use cases where latency, performance, or data privacy is a priority, but the FI lacks comfort with the public cloud or the necessary in-house expertise. The number of cloud leaders adopting “cloud first” is expected to increase from 37% of enterprises today to 50% by 2024

Finally, a minority of brokerage firms remain skeptical, showing no interest in migrating to the public cloud. External data sharing, cost, need for high-performance computing, and concerns about cloud service provider (CSP) lock-in are some of the top reasons skeptics are reluctant to move to the cloud.

Although approaches to cloud strategy vary, most take a federated approach, with a central center of excellence (COE). The COE, which is aligned with the architecture team, functions as a center of expertise and advice, providing flexibility to enterprise technology teams.

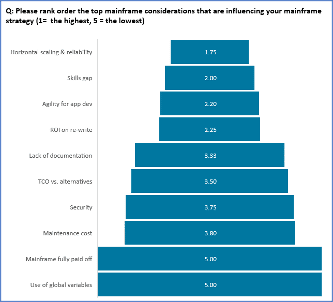

The gap is narrowing between the cloud and older computing platforms, including the mainframe. Mainframes remain prevalent in capital markets, with more than 50% (and 44 of the top 50 banks) still using a mainframe. Just over half (56%) plan to retire their mainframe, a process that will take five years or more; the remaining 44% will maintain and modernize it. Key considerations for strategic mainframe decisions focus on scaling, skills gap (which can be both a technology/resource issue and a business risk), and software development agility. ‘apps.

The number of companies that maintain their mainframes is perhaps surprising, but the reliance on mainframes stems from their remarkable functionality as workhorses, operating reliably, securely and quickly. Since the mainframe plays an ongoing role in supporting core processing, it is unlikely to go away. Instead, advances in technology (i.e. containerization of the mainframe) address key historical concerns, making it easier to support modern applications on the mainframe.

- Data exchange and data management

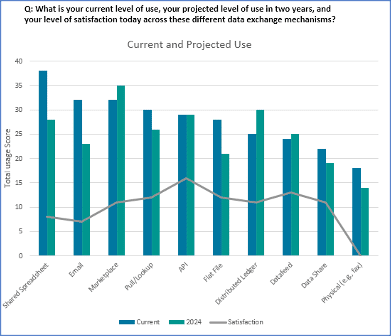

The area with the greatest potential for transformation is in data exchange mechanisms. Being a digital and data-driven organization enables the adoption of artificial intelligence (AI) approaches, including machine learning (ML), natural language processing (NLP), and deep learning.

Today, AI and the central domain of the data domain are approaching a significant change. Broad activation of data for insights requires effective enterprise data management; companies still have a lot of work to do in the areas of data exchange and data management to make this possibility a reality. Given this need, it’s no surprise that most companies (50%) identify themselves as being in the “early stages” of enterprise-wide AI adoption; 17% say they are developing their expertise with AI, and 33% say AI has been widely adopted. Typical use of AI today is in discrete (even mundane) domains, not enterprise use cases. Meanwhile, companies are evaluating a wide range of AI types, such as NLP for chatbot development, robotic process automation (RPA) for post-trade workflows, and optical character recognition ( OCR).

Manual and batch data exchange methods are hampering some data initiatives, but progress is expected in the next two years when real-time data transfer/exchange methods will dominate. Top drivers of data exchange efforts include speed and customer expectations/business drivers (both cited by 23% of respondents) and reliability and agility (tied at 14%). The growing use of data markets, distributed ledger technology (DLT) and application programming interfaces (APIs) are among the data-related technology approaches that are being heavily promoted.

Investment and adoption of APIs is expected to increase, as they received the highest rating for customer satisfaction, compared to a range of data exchange mechanisms ranging from more advanced approaches (like DLT and streams data) to legacy mechanisms (including manual approaches, such as fax). APIs have the ability to improve the customer experience through better access to features or data at a frequency that suits the customer.

Overcome obstacles

Securities firms face persistent challenges when adopting new technologies. For cloud initiatives, concerns include the expense of moving data to and from the cloud; storing data in the cloud without clear global location control can also run into regulatory hurdles related to privacy and data sovereignty. For mainframe initiatives, total cost of ownership (TCO) requires careful consideration of factors related to deployment models; the benefits (for availability, reliability, and security) can justify the expense of modernizing and retaining a mainframe rather than retiring it.

With respect to data exchange, full migration to contemporary data exchange methods is stalled due to the need to support customers who cling to older approaches. The poor state of data parks prevents the development of AI. While data sharing holds promise, the business case for true transformation in this area will require cross-industry coordination, as well as managing data privacy concerns.

Successful technology transformation in securities relies on understanding these barriers, adopting modern approaches, and making effective investments in technology innovation, enterprise-wide. Digital transformation requires moving beyond legacy technology parks to focus on customer centricity and customer activation.