ShyLama Productions/iStock via Getty Images

Introduction

Tourmaline oil (TSX:TOU:CA) (OTCPK: TRMLF) is one of the largest natural gas producers in Canada. Although the total production exceeds half a million barrels of oil equivalent per day and despite the word “oil” in the name of his company, almost 80% of his oil equivalent the production actually consists of natural gas, so we should really look at tourmaline from a natural gas perspective.

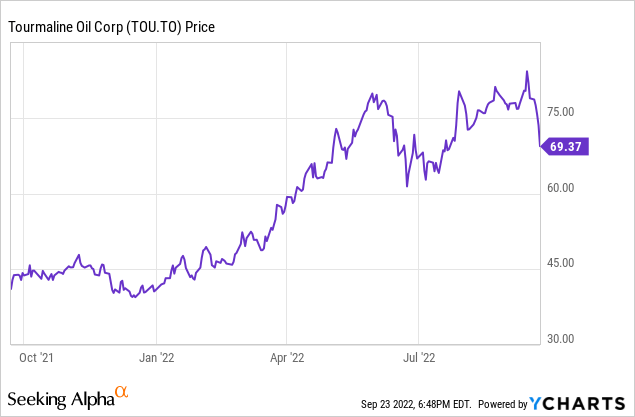

Although its American listing is relatively liquid with an average volume of nearly 50,000 shares per day (for a monetary value of US$2.5 million per day), the Canadian listing is obviously the most liquid since the average daily volume in Canada exceeds 2.3 million shares. . As Tourmaline publishes its financial results and has its most liquid listing in CAD, I will be using the Canadian dollar as my base currency throughout this article. The current market capitalization is approximately 23 billion Canadian dollars.

The first half was strong thanks to the high price of natural gas

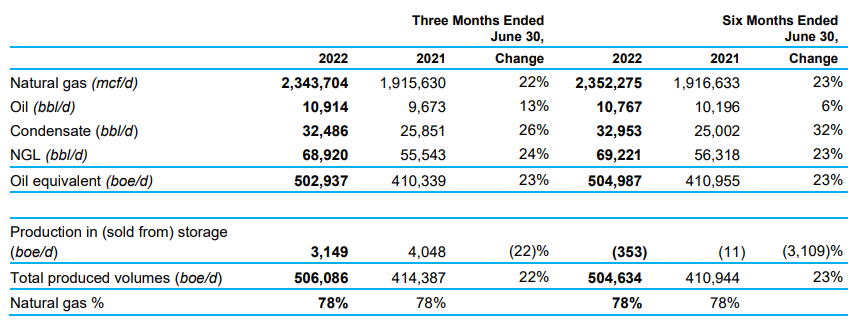

During the second quarter of this year, Tourmaline produced just over 500,000 barrels of oil equivalent per day. This is a slight decrease compared to the production rate of the first quarter of the year, but a substantial increase of 23% compared to the production rate of the same quarter last year, the assets and properties newly acquired having started to contribute.

Tourmaline Oil Investor Relations

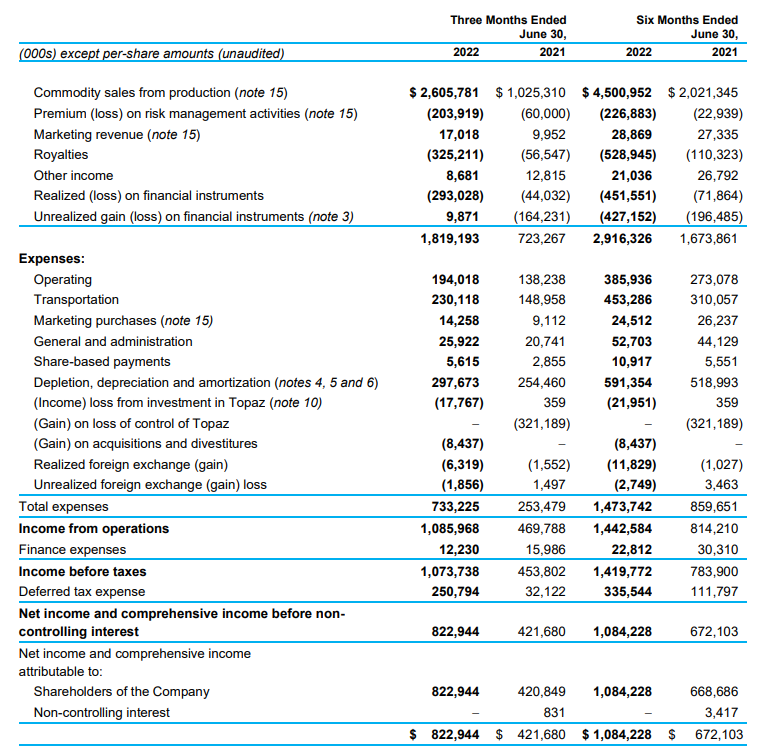

Total revenue in the second quarter was C$2.6 billion, and after taking into account royalty payments and hedging losses, net income was C$1.82 billion. Tourmaline has a very low operating cost as the total amount spent on the actual operation of the assets was just over C$730 million. Approximately 40% of operating expenses were made up of depletion and depreciation expenses.

Tourmaline Oil Investor Relations

Despite the nearly C$300 million in hedging losses, Tourmaline was still able to report a pre-tax profit of C$1.07 billion and a net profit of C$823 million, resulting in EPS of 2.46 Canadian dollars.

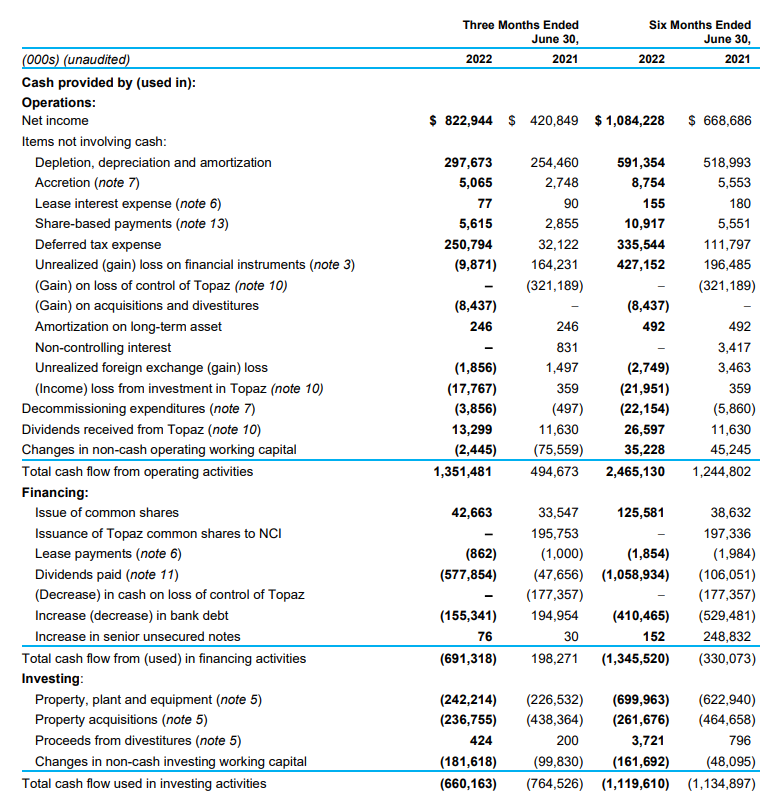

Looking at the cash flow statements, Tourmaline added approximately C$10 million of unrealized gains on the hedge portfolio to operating cash flow. In addition, the company will not have to pay taxes in the short term because it uses the tax pools available for Tourmaline. This boosted reported operating cash flow to C$1.35 billion.

Tourmaline Oil Investor Relations

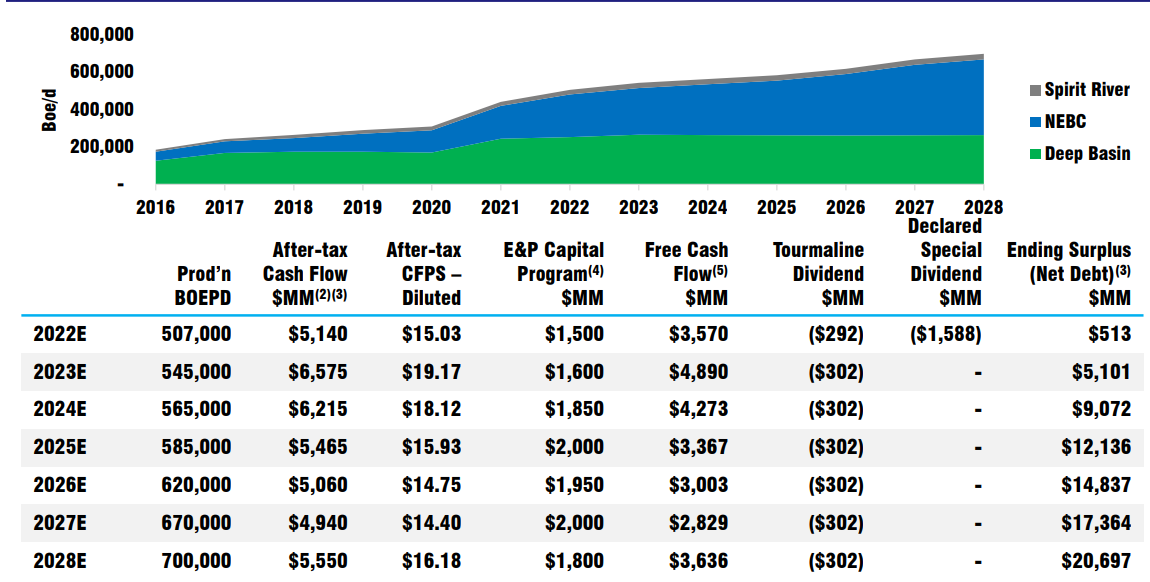

Total capital expenditure during the quarter was just C$242 million, meaning tourmaline generated approximately C$1.1 billion of free cash flow. Total free cash flow for the entire first half was approximately C$1.7 billion thanks to the ability to defer taxes. If Tourmaline had to pay taxes, adjusted free cash flow would have been approximately C$1.35 billion. The cash flow statement clearly shows that Tourmaline is generating more than enough cash flow to cover its planned annual investments, which should bring the production rate to 700,000 barrels of oil equivalent per day by 2028.

Tourmaline Oil Investor Relations

While we still have a full quarter to go in 2022, Tourmaline has already provided 2023 guidance

Earlier this month, Tourmaline already provided an update for 2023. The company expects to end 2023 with a total export of 925 mmcf per day, of which 140 mmcf per day exposed to the JKM price (LNG price in Asia) beginning January 1, 2023. For the full year, Tourmaline expects to produce 545,000 barrels of oil equivalent per day, which would represent an increase of approximately 7% from the forecast of 507,000 barrels of oil equivalent. oil equivalent per day that Tourmaline expects to produce this year.

The company has also started hedging its production for 2023 and while I know many oil and gas investors don’t like hedges, I think it’s a smart move to hedge some of the planned production to protect the cash flow. Tourmaline has already hedged approximately 26% of its expected natural gas production at a fixed price of C$5.26 per thousand cubic feet. A solid move as it will help the company increase its cash flow visibility for 2023. Additionally, some production that will correlate to the JKM price has also been hedged, at a price of US$50.46 per mmbtu.

Based on all of these, combined with per-band pricing for remaining production, Tourmaline now expects to generate approximately C$6.6 billion in operating cash flow in 2023. This represents an increase of 28 % vs. previous forecast of C$5.14 billion. Considering that the company plans to spend around C$1.6 billion on investments next year, Tourmaline is implicitly targeting a free cash flow result of C$5 billion.

Investment thesis

The third quarter could be slightly disappointing for Tourmaline as production will be lower than expected as the company voluntarily cut production while the Alberta/BC pipeline was down for maintenance. This shutdown had an immediate and substantial impact on the price of natural gas in Canada since the price of AECO natural gas was negative for several days in August. The lower production rate and lower spot prices probably mean that not too much should be expected from tourmaline in Q3, but cash flow will obviously remain very strong.

2023 is already looking very solid since the company has made the wise decision to cover part of its production. Add the 7% production increase and Tourmaline remains one of the biggest names in the North American natural gas industry.