Treasury yields have risen sharply in recent months. The yield on the last ten-year note issued, for example, rose from 1.73% on March 4 to 3.48% on June 14, reaching its highest level since April 2011. Rising yields lead to realized losses or at market value for fixed income investors. In this article, we place these losses in historical perspective and examine whether longer-term yield swings are best explained by higher short-term rate expectations or by investors demanding greater compensation for holding stocks. Treasury securities.

Increased yields = decreased yields

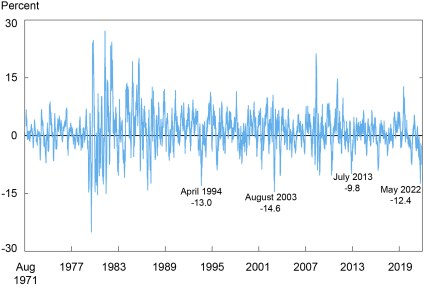

As yields and prices move in opposite directions, the recent sharp rise in yields has resulted in losses for owners of Treasuries. The chart below shows that returns based on the ten-year zero-coupon yield were -12.4% for the two-month (forty-two-day) period ending May 5. (All returns and yields in this article are nominal and therefore do not take inflation into account). The decline is the largest since August 2003 (-14.6%) and April 1994 before that (-13.0%).

Recent Treasury Yields Are Very Negative

Note: The chart represents the rolling two-month (forty-two trading day) cumulative returns of a hypothetical ten-year zero-coupon Treasury bond from August 16, 1971 through June 17, 2022.

Definition of liquidations

Since the duration of a liquidation in the bond market can be shorter or longer than two months, we take a flexible approach to defining liquidations. We first cumulate the returns of a hypothetical ten-year zero-coupon Treasury security from August 1971, identifying whenever the cumulative returns peak for the period to date. We then run through the data a second time, accumulating the returns from the maximum to date. Whenever a cumulative return falls below the maximum, we say a selloff has begun. When the cumulative return later reaches a new maximum, so that the losses are recouped, we say the sale is complete. We used a similar approach in our article looking at the 2013 sell-off from a historical perspective.

Our algorithm identifies forty-two sell-offs in which the cumulative yield of the ten-year zero-coupon bond falls below -5%. The average maximum cumulative loss for such sales is 11.1%, and the worst sale resulted in a loss of 38.4% (for an episode between June 1980 and August 1982). The average duration of a sale of 5% or more is 214 trading days (excluding the current sale, the end date of which is not yet known), the minimum is 21 days (for a episode between August and September 1982), and the maximum is 722 days (for an episode between July 2016 and May 2019).

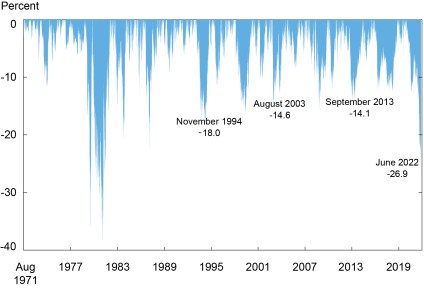

Largest current sale in 40 years

The graph below plots the sales, showing that the current sale is the largest in 40 years, surpassing those seen in 1994, 2003 and 2013. As of the date of publication, the bottom of the current sale occurred on the 14 June, with a cumulative return of -26.9%, compared to -14.1% in September 2013, -14.6% in August 2003 and -18.0% in November 1994. None of these episodes compares to the strong losses seen in the two Volcker-era liquidations of 1979-80 (-36.0%) and 1980-82 (-38.4%).

The current sale is higher than those observed in 1994, 2003 and 2013

Note: The chart represents the cumulative returns of a hypothetical zero-coupon ten-year Treasury bond during the bond market sell-offs, as defined in the text, between August 16, 1971 and June 17, 2022.

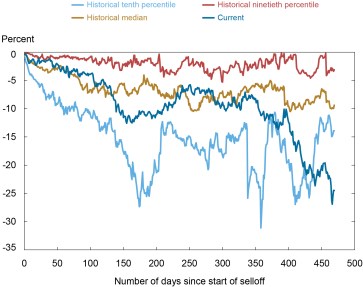

Sales pace comparable to others until recently

The following graph plots the cumulative returns of the current sale over time, against the distribution of returns from all previous sales over time. It shows that the current sale tracks the median of past sales at a comparable stage for the first 400 days, but then diverges. The recent divergence reflects the sharp rise in yields and fall in yields between March 4 and June 14.

Sales pace comparable to historical median until recently

Notes: The graph compares the cumulative returns during the event for the current sale with the distribution of cumulative returns for all sales (conditional on being sold for that many days) between August 16, 1971 and June 17, 2022. 450 days, the historical distribution is based on five massive sales.

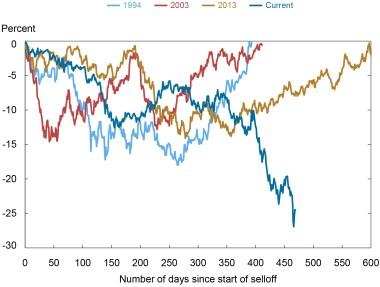

Sale duration longer than most

The chart below plots the cumulative returns of the current sell over time, against the sell in 1994, 2003, and 2013. The current sell diverges again most notably from the others after day 400. The chart also shows that the 1994 and 2003 sales ended around day 400, while the current one was rapidly worsening at this point. In fact, of the forty-one other sales since 1971 with cumulative returns of less than -5%, only five lasted 450 days, which is the duration of the current sale as of May 20.

The current liquidation lasts longer than the liquidations of 1994 and 2003

Note: The graph compares the cumulative returns during the event for the current sale with the sales for 1994, 2003 and 2013.

What explains the sale?

What explains the current sale? Do investors expect higher short-term rates than just a short time ago? Or can some or all of the rise in yields be explained by an increase in term premia, so that investors demand greater compensation for the risk of holding longer-term Treasuries? To answer these questions, we use estimates of ten-year zero-coupon term premia from Adrian, Crump, and Moench (2008) and, for each selloff, we aggregate returns that can be explained solely by variations term premium.

Our findings, presented in the chart below, suggest that the increase in yields in the first year or so of the current sell-off (from August 2020) may be explained by a rise in the term premium. In other words, cumulative returns based on the term premium alone (the red line) are of a similar magnitude to cumulative returns based on gross returns (the blue area). On the other hand, the growing negative yields since the end of 2021, amid growing prospects for monetary policy tightening, may be explained by expectations of higher short-term rates. The conclusion that the term premium changed only modestly once policy began to tighten in early 2022 is consistent with the evidence of past monetary tightening reported in this 2013 post.

Higher short-term rate expectations and term premia explain the current sell-off

Note: The graph plots the cumulative returns of a hypothetical zero-coupon ten-year Treasury bond during the bond market sell-off versus the cumulative returns during the sell-off attributable to changes in term premia for the period of sampling from August 16, 1971 to June 17, 2022. .

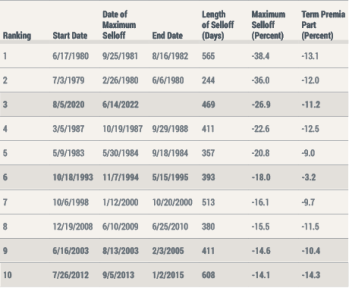

Liquidation Comparison

We list the characteristics of the ten biggest sell-offs in the bond market since 1971 in the table below. The four sales highlighted in this article – 1994, 2003, 2013 and 2022 – are ranked sixth, ninth, tenth and third respectively and highlighted with shading. Most of the sales, including the current sale, have a term premium component, although it is significantly lower than the sale as a whole. In contrast, the 2013 selloff stands out as having been driven entirely by changes in the term premium.

The current sale is the third largest since 1971

Notes: The table shows the characteristics of the ten largest liquidations in the bond market between August 16, 1971 and June 17, 2022. The figures in the last two columns reflect the period between the start date and the maximum liquidation date. Liquidations from 1994, 2003, 2013 and current are highlighted in shading.

When could the sale end?

According to our definition of a sell-off, the current sell-off will end when the cumulative returns since the start of the sell-off return to zero. Given that the selloff recently hit a new nadir of -26.9%, a sharp decline in yields would be needed to end the selloff anytime soon. This seems unlikely, in part given recent inflation readings and higher short-term rate expectations among policymakers and market participants. The sell-off would also eventually close even if yields did not change, as the return from holding Treasury securities ultimately offsets past capital losses. At the current level of interest rates (as of June 17, 2022), and assuming no further rate increases or rate decreases, our algorithm suggests that it would take investors approximately seven years to recover the losses accumulated since the start of the sale. .

Tobias Adrian is a Financial Advisor and Director of the Monetary and Capital Markets Department at the International Monetary Fund.

Michael J. Fleming is Head of Capital Markets Studies in the Research and Statistics Group at the Federal Reserve Bank of New York.

How to cite this article:

Tobias Adrian and Michael Fleming, “The Bond Market Selloff in Historical Perspective,” Federal Reserve Bank of New York Economy of Liberty StreetJuly 14, 2022, https://libertystreeteconomics.newyorkfed.org/2022/07/the-bond-market-selloff-in-historical-perspective/.

Disclaimer

The opinions expressed in this article are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Furthermore, the opinions expressed in this presentation are those of the authors and do not necessarily reflect the views of the International Monetary Fund, its management or its directors. Any errors or omissions are the responsibility of the authors.