South Korean banks have another six months to improve their near-term resilience to liquidity shocks as the country’s financial regulators focus on pumping more money into the market to ease a credit crunch.

Three of South Korea’s seven largest banks might have failed to meet the new minimum liquidity coverage ratio of 95%, down from 92.5% previously, if the Financial Services Commission, or FSC, had not delayed the deadline to meet the higher requirement. within six months to mid-2023, based on data from S&P Global Market Intelligence. The regulator said Oct. 20 that it would delay rolling back lower requirements announced during the COVID-19 pandemic to give banks more leeway to manage heightened volatility and uncertainty in the money market.

“Liquidity is tight in [South] Korea as the central bank raises its key rate,” said Michael Makdad, principal analyst at Morningstar. “I think the concern in Korea is about real estate properties. Some of these illiquid assets were funded with short-term debt.”

The country faces a delicate balancing act as authorities try to rein in inflation by raising interest rates and containing a credit crunch triggered by a Legoland theme park developer’s default. . Gangwon Jungdo Development Corp. missed 205 billion won in bond payments due on September 29, shaking money markets and forcing the Gangwon state government to promise it would cover the default, according to local media.

In the aftermath of the incident, more companies have struggled to refinance their maturing debts, particularly construction and power companies hit by rising global rates and commodity costs, in a amid sharply rising corporate bond yields and the cost of insuring debt against default.

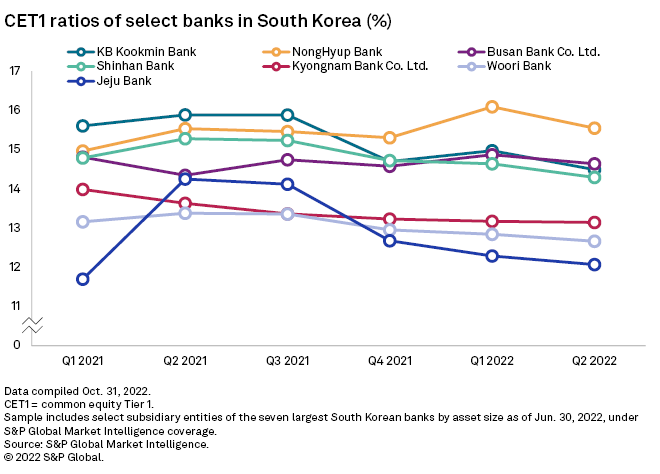

Among the seven largest local banks, KB Kookmin Bank failed to even meet the requirement to hold high-quality liquid assets equivalent to 92.5% of its total expected net cash outflows over the next 30 days, according to data from S&P Global Market Intelligence. Woori Bank was on the edge as of June 30, the data showed.

The extension of the deadline for banks to raise their liquidity coverage ratios to near pre-pandemic levels is part of South Korea’s effort to shore up the credit market. Other measures include raising the loan-to-deposit ratio ceiling and providing 50 trillion won in aid to help small businesses. A higher liquidity coverage ratio reduces the cash available in the secondary market, an impact that could be amplified during a credit crunch.

There are also concerns that banks could rush to sell bonds considered risky to shore up their liquidity position, which could further exacerbate credit market problems, two analysts told S&P Global Market Intelligence.

The failure of Legoland Korea Resort “has further weakened investor sentiment in the domestic debt capital market at a time when domestic interest rates have risen rapidly and the real estate market is weak,” said Daehyun Kim, director from S&P Global Ratings.

Market relief

Yields on AA-rated three-year corporate bonds fell to 5.37% on Dec. 5 after hitting a one-year high of 5.736% on Oct. 21, according to the Korea Financial Investment Association. Credit spreads between three-year corporate bonds and South Korean treasury bills of the same maturity stood at 176 basis points, down from 124 basis points on Oct. 21.

“We have asked large institutional investors to refrain from over-selling bonds or cutting back any projects [bond] purchases given the situation in the financial markets,” the FSC said in a statement on October 28.

KB Kookmin Bank, Woori Bank, Shinhan Bank Co. Ltd., NongHyup Bank, Busan Bank Co. Ltd. and Kyongnam Bank Co. Ltd. did not respond to a request from Market Intelligence. Jeju Bank could not be reached.

As of December 6, 1 dollar was equivalent to 1,319.48 South Korean won.