Quantitative funds are increasing their bets on U.S. stocks, helping fuel a strong rally that has added $7 billion in value to markets since June, even as economic data points to a slowdown in the world’s largest economy.

In many cases, funds – which look for market trends and then try to take advantage of momentum – quickly unwound positions taken in late 2021 and early this year that were structured to benefit from falling prices. stock markets.

By closing these bearish bets, they helped drive stock prices higher – and then followed the new trend by making new bets that profit from the rally.

Charlie McElligott, strategist at Nomura, said the quantitative funds “moved quickly and unemotionally” to change positions, catching “a very bearish market. . . very taken aback”.

Those funds have spent tens of billions of dollars on futures, helping to lift the benchmark S&P 500 and the Nasdaq Composite by double digits from recent lows, traders and analysts say.

Nomura estimates that trend-following hedge funds and volatility-control funds have bought $107 billion worth of global equity futures since markets bottomed in late June, much of which has been used for close short positions.

“With positioning essentially at the bottom, there was a lot of liquidity on the sidelines and so as the market stabilized and started to recover, more and more of that flow came back into the market,” said Glenn Koh. , responsible for stock trading. at Bank of America.

The role of computerized funds helps in part to explain the vertiginous rise of the US stock market by 47 billion dollars.

How long the “risk-on” shift lasts depends in part on the Federal Reserve’s ability to raise rates to dampen economic activity and stamp out inflation without pushing the world’s largest economy into recession.

Investors moved to the sidelines in droves as stocks tumbled earlier this year, and many trend-following hedge funds placed short bets on the market as they forecast further declines.

Markets were hit hard by Russia’s invasion of Ukraine in February, soaring commodity prices and the threat of economic slowdowns in China, the United States and Western Europe, just as central banks were raising interest rates to stifle inflation.

But after the S&P 500 fell into a bear market in June, the market rallied, recouping more than half of its losses this year.

Investors pointed to other factors propelling the rally in addition to the short-term squeeze that pushed some funds back into the market. Some managers are betting inflation could peak, while others argue that a surge of weak economic data could prevent the Fed from raising interest rates as aggressively as some policymakers believe.

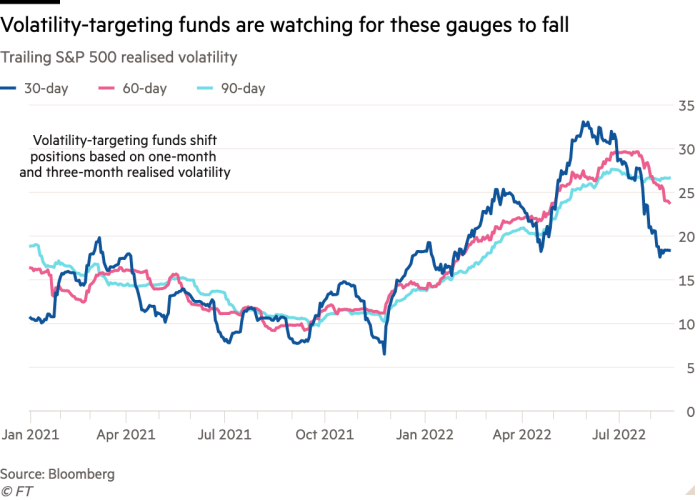

Along with the rally, the dramatic price swings that had characterized the selloff at the start of the year eased. Volatility gauges fell, with the Cboe’s Vix volatility index closing this month below its long-term average of 20 for the first time since April.

The daily swings of the S&P 500 and many of the stocks that make up the index have become weaker than they were between January and June. If this trend continues, the door will be open to a large pool of funds that switch positions based on volatility to increase their equity bets.

JPMorgan Chase analysts said the buying could continue. He told his hedge fund clients last week that volatility targeting and risk parity funds were buying about $2 billion to $4 billion worth of stocks a day. The bank estimated that these purchases “could possibly last another 100 days if volatility remains low”.

Marko Kolanovic, a JPMorgan strategist, said the rally has reached most corners of the market. Some 88% of S&P 500 stocks are trading above their average over the past 50 days, down from just 2% in mid-June.

“A strong turnout is an indication that this rally is sustainable, and another expression that extreme market risks have receded,” Kolanovic said. “Volatility targeters can be expected to increase overall exposure, and in particular to equities.”

Fund managers have become more optimistic. After polling portfolio managers this month, Bank of America strategist Michael Hartnett said they were “no longer apocalyptically bearish.”

Big caveats remain. Fed policymakers have warned they could raise rates higher and hold them longer than traders currently expect. And an inflation or growth shock could still shake the markets.

This explains why the rally has so far been driven by systematic funds rather than traditional fund managers and long-short equity hedge funds.

“You see some people taking shorts,” said Mike Lewis, head of U.S. cash equity trading at Barclays. “But you haven’t really seen people taking money and putting it back to work.”

Quantitative funds are increasing their bets on U.S. stocks, helping fuel a strong rally that has added $7 billion in value to markets since June, even as economic data points to a slowdown in the world’s largest economy.

In many cases, funds – which look for market trends and then try to take advantage of momentum – quickly unwound positions taken in late 2021 and early this year that were structured to benefit from falling prices. stock markets.

By closing these bearish bets, they helped drive stock prices higher – and then followed the new trend by making new bets that profit from the rally.

Charlie McElligott, strategist at Nomura, said the quantitative funds “moved quickly and unemotionally” to change positions, catching “a very bearish market. . . very taken aback”.

Those funds have spent tens of billions of dollars on futures, helping to lift the benchmark S&P 500 and the Nasdaq Composite by double digits from recent lows, traders and analysts say.

Nomura estimates that trend-following hedge funds and volatility-control funds have bought $107 billion worth of global equity futures since markets bottomed in late June, much of which has been used for close short positions.

“With positioning essentially at the bottom, there was a lot of liquidity on the sidelines and so as the market stabilized and started to recover, more and more of that flow came back into the market,” said Glenn Koh. , responsible for stock trading. at Bank of America.

The role of computerized funds helps in part to explain the vertiginous rise of the US stock market by 47 billion dollars.

How long the “risk-on” shift lasts depends in part on the Federal Reserve’s ability to raise rates to dampen economic activity and stamp out inflation without pushing the world’s largest economy into recession.

Investors moved to the sidelines in droves as stocks tumbled earlier this year, and many trend-following hedge funds placed short bets on the market as they forecast further declines.

Markets were hit hard by Russia’s invasion of Ukraine in February, soaring commodity prices and the threat of economic slowdowns in China, the United States and Western Europe, just as central banks were raising interest rates to stifle inflation.

But after the S&P 500 fell into a bear market in June, the market rallied, recouping more than half of its losses this year.

Investors pointed to other factors propelling the rally in addition to the short-term squeeze that pushed some funds back into the market. Some managers are betting inflation could peak, while others argue that a surge of weak economic data could prevent the Fed from raising interest rates as aggressively as some policymakers believe.

Along with the rally, the dramatic price swings that had characterized the selloff at the start of the year eased. Volatility gauges fell, with the Cboe’s Vix volatility index closing this month below its long-term average of 20 for the first time since April.

The daily swings of the S&P 500 and many of the stocks that make up the index have become weaker than they were between January and June. If this trend continues, the door will be open to a large pool of funds that switch positions based on volatility to increase their equity bets.

JPMorgan Chase analysts said the buying could continue. He told his hedge fund clients last week that volatility targeting and risk parity funds were buying about $2 billion to $4 billion worth of stocks a day. The bank estimated that these purchases “could possibly last another 100 days if volatility remains low”.

Marko Kolanovic, a JPMorgan strategist, said the rally has reached most corners of the market. Some 88% of S&P 500 stocks are trading above their average over the past 50 days, down from just 2% in mid-June.

“A strong turnout is an indication that this rally is sustainable, and another expression that extreme market risks have receded,” Kolanovic said. “Volatility targeters can be expected to increase overall exposure, and in particular to equities.”

Fund managers have become more optimistic. After polling portfolio managers this month, Bank of America strategist Michael Hartnett said they were “no longer apocalyptically bearish.”

Big caveats remain. Fed policymakers have warned they could raise rates higher and hold them longer than traders currently expect. And an inflation or growth shock could still shake the markets.

This explains why the rally has so far been driven by systematic funds rather than traditional fund managers and long-short equity hedge funds.

“You see some people taking shorts,” said Mike Lewis, head of U.S. cash equity trading at Barclays. “But you haven’t really seen people taking money and putting it back to work.”