The collapse of FTX has reignited the narrative that “Bitcoin maximalists were right all along.”

Given the size of the struggling exchange and the number of entities caught up in its network, the FTX scandal has been in the headlines lately.

Worse, each passing day seemingly brings new twists that point to serious failings within the company and among the regulators that were supposed to prevent such scandals from happening in the first place.

In particular, questions hang over Sam Bankman-Fried’s (SBF) political influence and connections, as well as FTX’s apparent “pass” with the Securities and Exchange Commission (SEC).

Behind the veil of sports endorsements and high-profile celebrities, FTX has managed to build a trusted reputation in its relatively short three and a half years of existence. Although skeptics said the red flags were still there, that’s no consolation for those who bet on FTX and lost big.

At the heart of the scandal is FTX’s native FTT token and how it was handled. During a liquidity stress test, it failed to justify its lofty market cap valuation of $3.4 billion before the crash.

The net result of the scandal is the loss of billions and an industry scrambling to preserve what little reputation and credibility remains.

Undoubtedly, the bankruptcy spawned a new wave of Bitcoin maximalism, and as some might say, their vitriol towards sh*tcoins has proven time and time again.

Bitcoin self-custody as an answer

The leading cryptocurrency is simple in design and, by all accounts, a dinosaur in terms of technology. However, maxis points out that these same “loopholes” are what make Bitcoin the only digital asset to hold.

On the basis that Bitcoin has no oversight foundation, twisted incentives, or groups with special rights, the maxis argue that the principles of decentralization, transparency, and immutability only apply to BTC.

Passionately advocating this view, the Bitcoin-only crowd has been called toxic and narrow-minded in the past. Still, the events of the past week demonstrate some degree of truth, at least from the perspective of anti-ponzinomics applied to exchange tokens.

Blow after blow from Celsius, BlockFi, Voyager, Terra Luna, etc., the penny begins to drop. Trust, simplicity and honesty trump performance and short-term gain.

As the industry emerges from the FTX black swan, the BTC maxi movement will only get stronger.

Altcoins are “bad”

On-chain analyst Jimmy Song wrote a lengthy piece on the “moral case against altcoins.” He covered a range of points against altcoins, including falsely exploiting the legitimacy of BTC and the influence of short-term VC incentives.

He argued that “altcoins are bad” and simply mirror the fiat system but in a new package. With that, their proliferation will not lead to financial freedom, as is often the goal of many entering the crypto space. On the contrary, the existence of altcoins only confuses cryptocurrency from the point of view of obtaining the real thing, i.e. Bitcoin.

Additionally, Song argued that the altcoin space is hindering the adoption of Bitcoin, preventing those who need it most from acquiring it due to the focus on new, brighter projects.

“Altcoins are a cesspool of theft, cronyism, and rent seeking. Altcoins build on the reputation Bitcoin has worked hard to achieve. They enrich VCs and altcoins at the expense of the poor and vulnerable.

Most would have called these views extreme in the past, or perhaps too black and white. However, the ongoing CeFi scandals this year have made more people accept these points.

On-chain data shows penny dropped

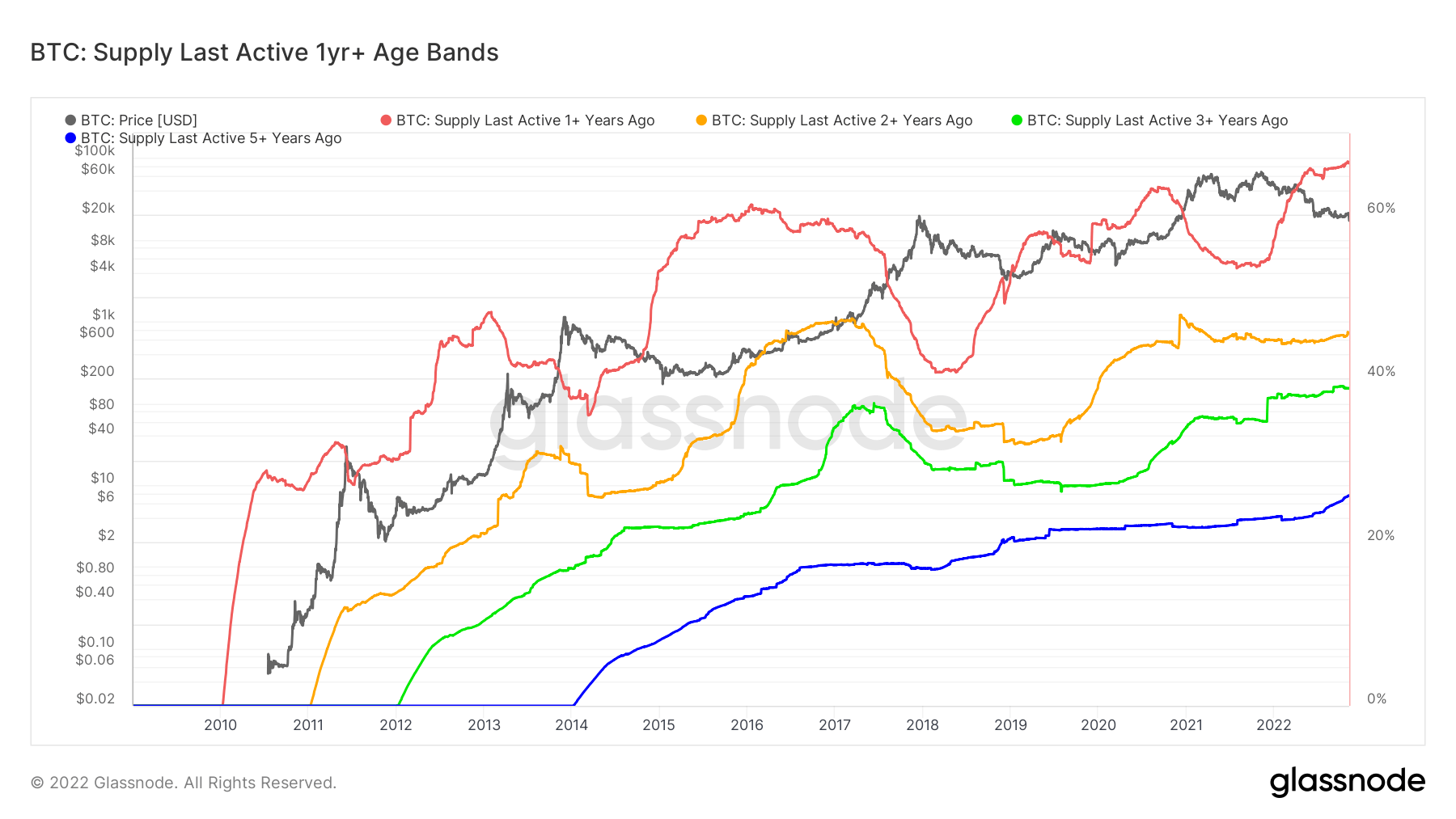

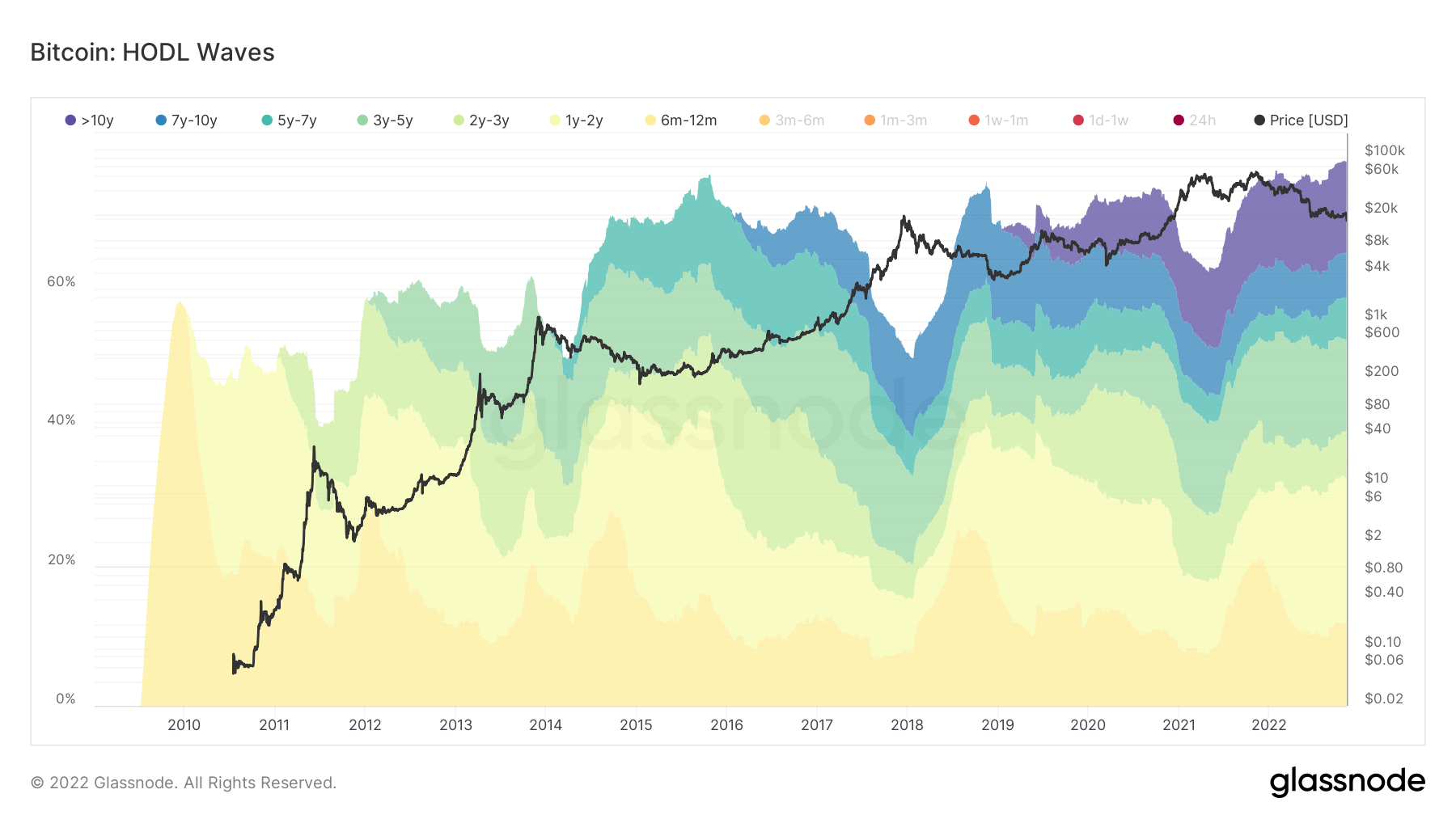

Despite the selling pressure impacting the price of Bitcoin in the immediate term, long-term HODLers continue to believe.

The HODL Waves chart shows the amount of BTC in circulation broken down into age bands representing the last shift in supply.

The chart below shows a sharp rise in the over 10 age bracket. This has been a noticeable trend since around 2020. However, the >10 year wave continues to widen as the price of BTC declines.

In addition, the total of the age groups combined reaches 76% – a new all-time high.

Analysis of active offer over broader time frames shows a general upward trend in all categories longer than one year. The most active group since 2022 is the red group 1+ years ago, suggesting that relatively recent participants are maxing out.