Torsten Asmus

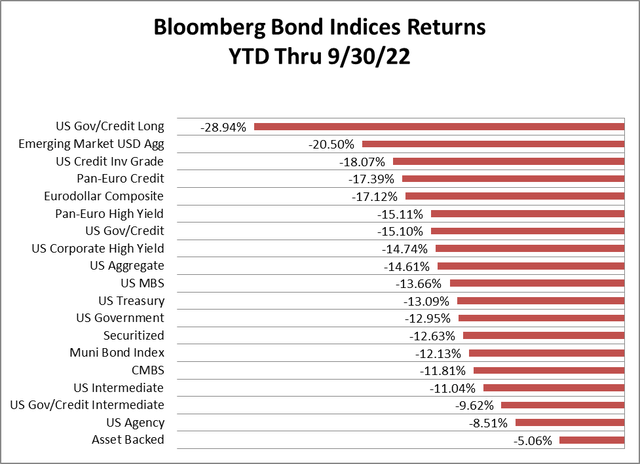

2022 has proven to be a tough year for bond investors. The broadest measure of the bond market, the Bloomberg US Aggregate Index, returned -14.61% through the end of the third quarter. There was no place to hide, as all segments of the bond market have experienced negative returns since the beginning of the year. Asset-backed securities (ABS) had the best performance with a return of -5.06%, while the US Govt/Credit Long segment had the worst performance with a return of -28.94%.

These results are not surprising, as ABS represents the shortest component of the aggregate index, with a duration of 2.16 years, while the US Govt/Credit Long segment represents the longest component of the index. aggregate, with a duration of 14.30 years.

This is shaping up to be the worst year of performance in the aggregate index’s 45-year history. The previous largest drop was -2.92 in 1994. Using a broader data series compiled by NYU, 2022 appears to be the worst year since 1931.

Bloomberg

The reason bonds have performed so poorly is due to the sharp rise in interest rates in 2022.

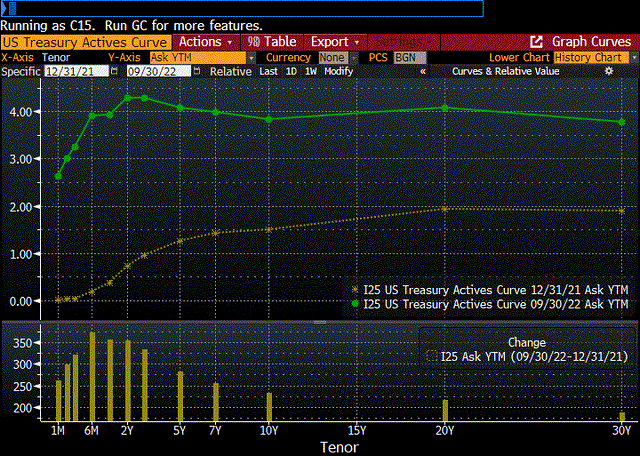

Rates rose across the yield curve, with the biggest jump occurring on 6-month Treasury bills, with the yield rising 372 basis points (bps) to 3.90%. The weakest gain occurred at the long end of the curve, with 30-year US Treasury bonds rising 187 basis points to 3.78%.

Bloomberg

The larger gains at the front end of the curve caused the yield curve to invert, with the highest point on the curve being the 2-year US Treasury at 4.28%.

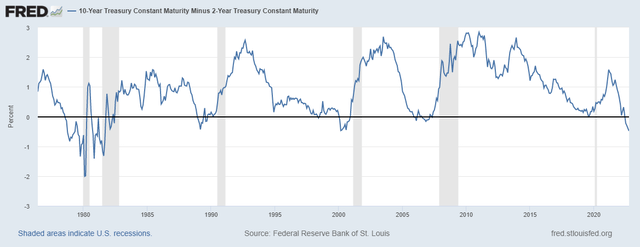

The yield curve is often a good predictor of an economic recession. When the curve, as measured by the spread between the 2-year US Treasury note and the 10-year US Treasury note, inverts, recession often ensues. At the end of the quarter, the 2-10 year curve was inverted by 45 basis points. Yield curve inversion has preceded every recession since 1980.

However, there is usually a 12 to 24 month lag between the inversion of the yield curve and the onset of a recession.

Fred

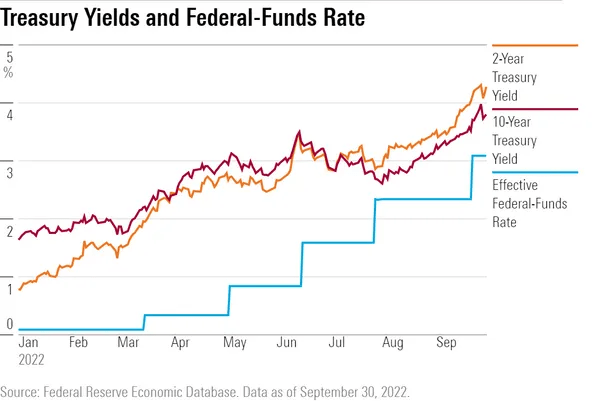

Rates have risen dramatically this year as the Fed tightened monetary policy in an effort to contain the highest inflation rate in 40 years. Since the beginning of the year, the Fed has increased its benchmark Fed Funds rate 5 times by a total of 300 basis points to reach the current range of 3.00 to 3.25%. This tightening should continue.

Fred

The Fed faces the difficult task of trying to bring inflation back to its long-term target of 2% without causing a recession. Fed Chairman Jay Powell acknowledged that this will be a difficult task. It is prepared to tolerate a modest increase in unemployment until there is clear evidence that inflation is moving back towards its target.

In addition to raising its benchmark rate, the Fed is also embarking on its previously announced balance sheet reduction, otherwise known as quantitative tightening (QT). This is another step in normalizing their post-pandemic policy. Although first announced in November 2021, the balance sheet reduction has been rolled out gradually. In January 2022, the FOMC announced its intention to reduce holdings of Fed securities over time in a predictable manner. Beginning in June 2022, maturities of Treasury securities and MBS held in the Fed’s SOMA wallet were allowed to be canceled subject to a cap of $47.5 billion per month. In September 2022, this cap was increased to a total of $95 billion per month.

Currently, the Fed is the world’s largest owner of US Treasury and MBS securities, holding $5.7 trillion and $2.7 trillion, respectively. They have been the marginal bid for these bonds for the past two years, and their absence will continue to put pressure on markets going forward.

While many see signs that inflation may have peaked and predict that the Fed could soon change course, Powell insisted that “history strongly warns against premature policy easing. “.

According to Rick Rieder, CIO of Global Fixed Income at BlackRock, in a recent interview with Barron, “Buying the dip doesn’t work during QT; you keep getting new dips.

There is consolation to higher rates since the Fed started to tighten. Cash, which has offered virtually no yield for several years, is now attractive. Yields on money market funds are approaching 3%, the highest level in 14 years, and one-year US Treasuries are yielding more than 4%. These are safe alternatives to avoid bond volatility.

Torsten Asmus

2022 has proven to be a tough year for bond investors. The broadest measure of the bond market, the Bloomberg US Aggregate Index, returned -14.61% through the end of the third quarter. There was no place to hide, as all segments of the bond market have experienced negative returns since the beginning of the year. Asset-backed securities (ABS) had the best performance with a return of -5.06%, while the US Govt/Credit Long segment had the worst performance with a return of -28.94%.

These results are not surprising, as ABS represents the shortest component of the aggregate index, with a duration of 2.16 years, while the US Govt/Credit Long segment represents the longest component of the index. aggregate, with a duration of 14.30 years.

This is shaping up to be the worst year of performance in the aggregate index’s 45-year history. The previous largest drop was -2.92 in 1994. Using a broader data series compiled by NYU, 2022 appears to be the worst year since 1931.

Bloomberg

The reason bonds have performed so poorly is due to the sharp rise in interest rates in 2022.

Rates rose across the yield curve, with the biggest jump occurring on 6-month Treasury bills, with the yield rising 372 basis points (bps) to 3.90%. The weakest gain occurred at the long end of the curve, with 30-year US Treasury bonds rising 187 basis points to 3.78%.

Bloomberg

The larger gains at the front end of the curve caused the yield curve to invert, with the highest point on the curve being the 2-year US Treasury at 4.28%.

The yield curve is often a good predictor of an economic recession. When the curve, as measured by the spread between the 2-year US Treasury note and the 10-year US Treasury note, inverts, recession often ensues. At the end of the quarter, the 2-10 year curve was inverted by 45 basis points. Yield curve inversion has preceded every recession since 1980.

However, there is usually a 12 to 24 month lag between the inversion of the yield curve and the onset of a recession.

Fred

Rates have risen dramatically this year as the Fed tightened monetary policy in an effort to contain the highest inflation rate in 40 years. Since the beginning of the year, the Fed has increased its benchmark Fed Funds rate 5 times by a total of 300 basis points to reach the current range of 3.00 to 3.25%. This tightening should continue.

Fred

The Fed faces the difficult task of trying to bring inflation back to its long-term target of 2% without causing a recession. Fed Chairman Jay Powell acknowledged that this will be a difficult task. It is prepared to tolerate a modest increase in unemployment until there is clear evidence that inflation is moving back towards its target.

In addition to raising its benchmark rate, the Fed is also embarking on its previously announced balance sheet reduction, otherwise known as quantitative tightening (QT). This is another step in normalizing their post-pandemic policy. Although first announced in November 2021, the balance sheet reduction has been rolled out gradually. In January 2022, the FOMC announced its intention to reduce holdings of Fed securities over time in a predictable manner. Beginning in June 2022, maturities of Treasury securities and MBS held in the Fed’s SOMA wallet were allowed to be canceled subject to a cap of $47.5 billion per month. In September 2022, this cap was increased to a total of $95 billion per month.

Currently, the Fed is the world’s largest owner of US Treasury and MBS securities, holding $5.7 trillion and $2.7 trillion, respectively. They have been the marginal bid for these bonds for the past two years, and their absence will continue to put pressure on markets going forward.

While many see signs that inflation may have peaked and predict that the Fed could soon change course, Powell insisted that “history strongly warns against premature policy easing. “.

According to Rick Rieder, CIO of Global Fixed Income at BlackRock, in a recent interview with Barron, “Buying the dip doesn’t work during QT; you keep getting new dips.

There is consolation to higher rates since the Fed started to tighten. Cash, which has offered virtually no yield for several years, is now attractive. Yields on money market funds are approaching 3%, the highest level in 14 years, and one-year US Treasuries are yielding more than 4%. These are safe alternatives to avoid bond volatility.