Investment thesis

The rapid correction in stocks last week saw investors abandon virtually all risky assets, even low volatility stocks and gold. The only asset class with strong returns was Treasury bills. While government bonds are a natural landing point in a fast-paced “safety hiding” environment, I want to explain why investment grade short-term corporate bonds still make a good choice despite the recent pivot of risk.

Context

The sudden correction in the market last week reminds us why it is important to keep in mind the defensive positioning of the portfolio, even if it seems that the Fed’s money printing machine will cure all our ills. Although we may sometimes witness an economic contraction to come, black swan events, such as the coronavirus, arrive with little warning but can have a significant impact.

A few weeks ago, I wrote about the iShares Short Maturity Bond ETF (NEAR) and how it can be used both as a quasi-monetary alternative in a portfolio or as a diversification tool to round out the long-term portfolio risk. It turned out to be one of my most popular articles in recent memory and the comment thread (over 160 in all) mentioned a number of similar fixed income ETFs that could serve a similar purpose.

The one I want to watch today is the PIMCO Enhanced Short Maturity Active (MINT) ETF. Like NEAR, it focuses on high-quality short-term corporate bonds with variable maturities and whose overall portfolio duration is less than one year. I find this duration range to be an ideal target for conservative fixed income investors, as it offers a solid combination of above-average dividends with minimal additional risk.

Overview

MINT is an actively managed, ultra-short-term investment grade corporate bond fund that aims to maintain an overall portfolio life of less than one year. PIMCO itself describes MINT as a cash alternative and I agree with its viability as such. In its current version, MINT has an overall life of only 0.25 years. Compared to a money market and its stable share price at $ 1, it carries very little additional interest rate risk, an attractive characteristic for income seekers who seek to improve their risk / return profiles. .

In the current environment where the Fed is expected to continue lowering interest rates throughout the year, MINT may be able to tackle a modest appreciation in stock prices in addition to the rise in yield.

Source: PIMCO

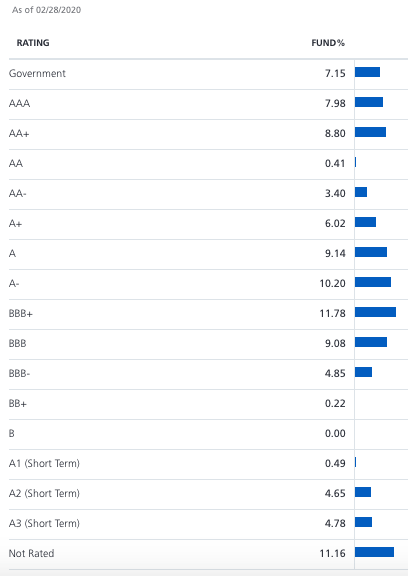

I have noted several times in recent months that investors should completely avoid the high yield bond space and focus only on higher quality fixed income. MINT completely avoids high yield bonds and the hatching of government bonds it holds in the portfolio (around 7% of assets) contributes to improving the overall quality of credit. “Other net short-term instruments” mainly included cash positions and bonds not rated in the portfolio.

Like many other premium bond portfolios, MINT is overweight in the BBB category, but not to the extent that I believe it is exposed to undue risk.

Source: PIMCO

The 25% allocation to BBB rated bonds actually compares favorably to other corporate bond ETFs. The iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), one of the largest bond funds in the sector, holds almost half of its assets in the BBB compartment and 40% in A-rated bonds.

Most of these funds retreat into lower quality bonds in order to increase yield, but in the current economic environment, I would much prefer that MINT favor a higher credit quality, even if this is to the detriment of the yield.

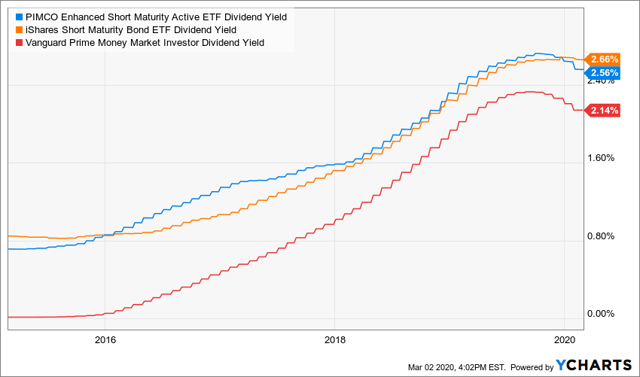

By putting MINT, NEAR and the Vanguard Prime Money Market Fund (VMMXX) side by side, we see that the recent pivot of MINT towards a more conservative allocation has cost it a return.

It may be misleading to look at returns at 12 months of follow-up, as much of that return was earned in a higher rate environment. As for current yields, MINT is 1.77%, NEAR is 2.00% and VMMXX is 1.60%.

Again, this is a case where MINT maintains a more conservative credit profile. Although NEAR also maintains a first-class profile, it holds around 42% of the assets in BBB-rated bonds, compared to only 25% for MINT.

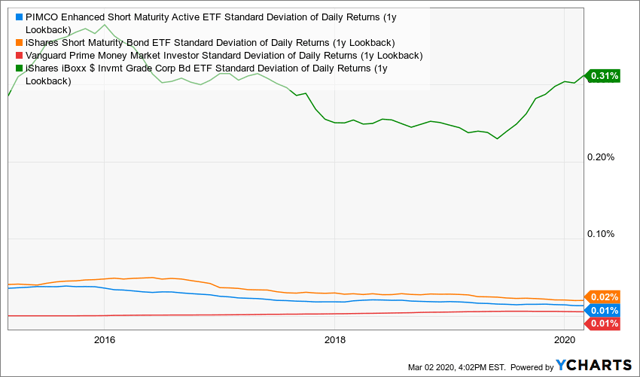

MINT may have a relatively modest 0.17% return bonus compared to the money market fund at this time, but this increase in returns is also accompanied by a negligible additional level of risk.

MINT has always been in the ultra-low risk category, but its recent move towards higher quality places it in a rounding error in the average risk level of a money market fund. The standard deviation of LQD returns is also shown on the graph for comparison.

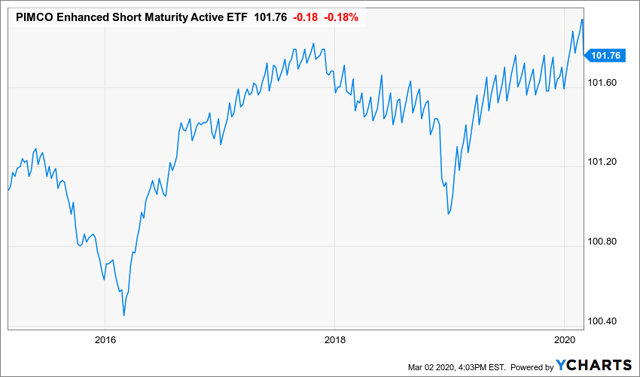

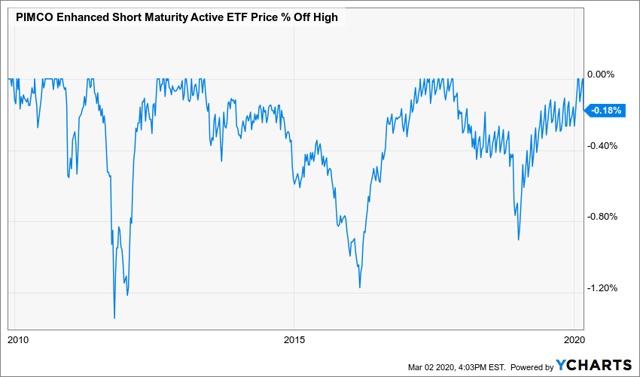

Since the industrial recession of 2016, MINT’s share price has remained stable in the range of $ 101. Of course, since it is a portfolio of corporate bonds exposed to credit risk, its value will tend to fall under more difficult market conditions, as was the case in 2015/2016 and again at the end 2018.

Historically, however, the fall in MINT’s share price has been relatively limited. Just three times in the past decade, the maximum circulation has reached more than 0.8%.

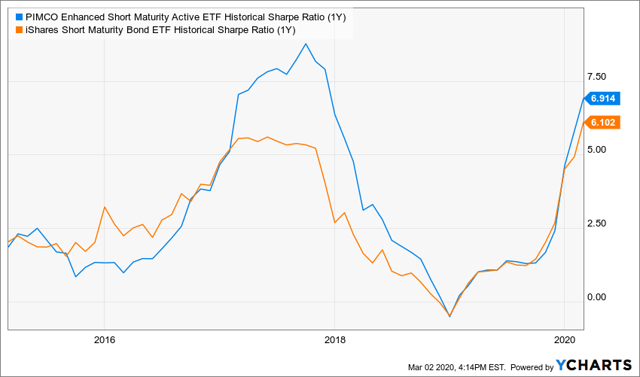

Looking to explain why you might want to choose MINT over a peer like NEAR? While the two tend to be similar in terms of portfolio composition and risk, risk-adjusted returns in recent years have been higher for MINT.

Of course, this could be the case for one or the other depending on your objective. Investors looking for better risk-adjusted returns may prefer MINT, while seekers of purer returns may opt for NEAR. I think you can argue for NEAR as long as the performance bonus remains above this 0.2% level. Less than that and there may not be a huge benefit.

Conclusion

With a peak in volatility and the VIX regularly residing above level 30, the time has come to think about asset protection rather than asset growth. For most people, this means diving into treasury bills and gold, but that doesn’t have to be the case.

Premium quality, very short duration corporate bonds are still acceptable in this environment as long as the focus is on quality and risk is minimized. The recent focus of MINT on increasing the quality scale in A-rated bonds makes it a better choice in a volatile market while not sacrificing too much in terms of yield.

With 10-year T-Bill yields now below the 1% level, don’t worry about adding low-risk, high-quality, short-term corporate bonds to your portfolio as an enhancer. yield.

Disclosure: I am / we are a long time VMMXX. I wrote this article myself and it expresses my own opinions. I do not receive any compensation for this (other than from Seeking Alpha). I have no business relationship with a company whose actions are mentioned in this article.