cagkansayin

Co-produced with Treading Softly

Look at your trash can. Is it full or empty? How about the one outside your house? How full is it? Do you refill it weekly or does it usually stay empty?

Trash can. It’s something our current society generates tons of. In fact, thousands of tons of trash end up in landfills every year. Taking otherwise useful space and creating large man-made artificial mountains.

Why not burn it? “Oh, it’s bad for the environment!” you might say, but isn’t it bad for the environment to leave trash in massive piles – every time it rains chemicals and such leak into the ground and into the water table.

Interestingly, Waste-To-Energy technology has been around for decades, but lately it has gained momentum as a “renewable” source of energy. Carbon capture technology has improved over time, and through an efficient combustion process, waste can be easily converted into energy to power homes.

A leader in this space is Babcock & Wilcox Enterprises (New York Stock Exchange: BW). BW does not pay a dividend on its common stock. While others might invest in it anyway just because they like its environmental focus, not having a dividend is a business killer for us. We are income investors looking for a source of income to fuel our lifestyles.

So where can we find it with BW? When you like a company, but it’s not paying dividends, look higher up the capital stack. BW has two attractive baby bonds that will provide us with income and a higher position in the capital structure to boot!

Let’s take a closer look at this long-standing American company.

What are they doing?

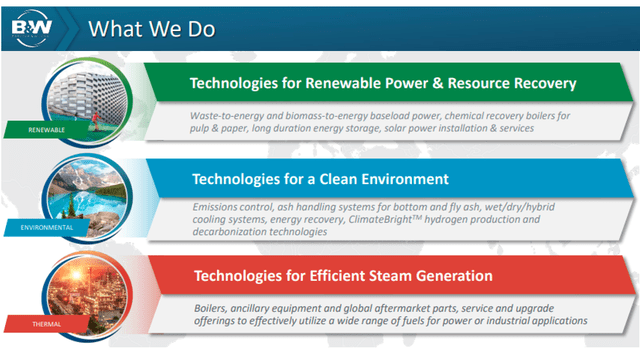

BW is divided into three main reporting segments.

Babcock & Wilson Earnings Slides

These segments are renewable, environmental and thermal. BW’s primary growth focus is currently its renewable energy segment, which has recently been its engine of revenue growth.

Essentially, their segments work hand in hand, but can also be used piecemeal by third parties.

BW’s renewable energy segment has seen the fastest growth in recent times. Renewable technologies are all the rage these days – how many publicly traded solar panel companies have come and gone? However, BW does not focus on mining sites. BW’s role is to build the projects that other companies like NextEra Energy Partners (NEP) would own and operate. Thus, the growing demand for solar energy to be built benefits BW.

Their waste-to-energy and renewable biomass projects continue to attract attention and strengthen their backlog. BW is primarily a builder and repairer of power plants, not the operator. Thus, their revenues will be lump sum depending on the start and end of the projects, but they do not bear the costs or risks associated with the operation of the power plants.

BW’s Environment segment focuses on carbon capture and similar technologies. These are added to currently operating facilities or built adjacent to newly constructed locations.

The Thermal segment focuses on the boiler itself and the associated infrastructure. Most power plants still focus on the age-old methodology of heating water to steam and turning large turbines to generate electricity. Means of heating water can vary – coal, biomass, nuclear, etc. – but the need for a turbine and a boiler with associated pipes is universal. BW builds, upgrades and maintains this infrastructure for power plants and industrial furnaces around the world.

Balance sheet

BW is going through a corporate revitalization. For a time, BW’s financial health and earnings struggled to find a solid footing as the company invested heavily in the renewable/environmental side of its business. It often takes time for new investments to start paying off, which can mean a tough time. This is now starting to reward them as their project backlog has grown and new income is coming in.

Looking for Alpha

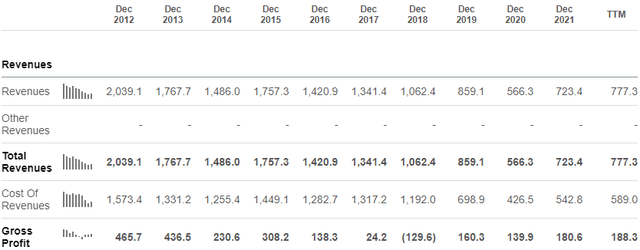

Over the past ten years, BW saw revenue decline and profits turn negative in 2018 before recovering. Currently, BW generates similar profits with less revenue. Their shift in focus produced higher margin business.

To survive this season of changes and difficulties. BW was forced to tap into the capital markets. They’ve done it three times through 2021, issuing two baby bonds and one preferred. They did so in 2021 to repay other loans and clean up their balance sheets. That effort left them with $334.3 million in debt and $100 million in preferred stock.

Their adjusted EBITDA of $32 million for the first six months of 2022 provides an interest coverage ratio of 1.49x, this is a significant improvement over the first six months of 2021, which had a ratio of interest coverage of only 1.07x.

We expect their coverage ratio to continue to climb over the coming quarters as activity picks up. BW has over $7.5 billion in its pipeline, excluding parts and service. (Source: B&W Investor Presentation)

B7W August Presentation

This will lead to a significant increase in revenue and EBITDA. BW ended 2021 with a coverage ratio of 1.79x, and we expect it to be similar for 2022 or more.

It pays to be a bondholder

When it comes to revenue, we prefer to be first in line to get paid. With BW, we see two great ways to get paid:

- Babcock & Wilcox Enterprises, Inc. 6.50% Senior Notes due 12/31/2026 (NYSE: BWNB) – Yield to maturity 8.7%

- Babcock & Wilcox Enterprises, Inc. 8.125% Senior Notes due 02/28/2026 (NYSE: BWSN) – Yield to maturity 9.3%

Both are great sources of income, but at the time of writing, BWSN is more attractive with a higher YTM. However, either baby bond is a great source of income until 2026. BWSN has already passed its call date (and will tend to trade closer to face value). However, the current redemption price would be $25.75, and it drops by $0.25 each February until it reaches $25.00 in February 2025.

BWNB has a different prepayment option, which is detailed in the prospectus. If called before the par call date of 2026, a Make-Whole provision requires payment of the present value of the remaining scheduled interest payments.

What about their preferred stock? Babcock & Wilcox Enterprises, Inc. 7.75% Series A Cumulative Preferred Stock (BW.A) has a current yield of around 9% and becomes redeemable in May 2026. This current yield may be attractive, but BWNB and BWSN have a much higher degree of security and a similar YTM offered than the risky BW higher. -A. Preferred stocks pay a qualified dividend if held in a taxable account (whereas bonds pay interest). If you can get a similar return with the lower risk of a bond, go for the lower risk!

Shutterstock

Conclusion

BW underwent a heavy transition and change in focus. Bankruptcy risks are now well anchored in hindsight. BW management has executed effectively to eliminate other more expensive debt by issuing two baby bonds and one preferred stock through 2021.

While BW common stock can be a wild ride without the reward of a strong common dividend, we can see that climbing higher up the capital stack, skipping over preferred stock and moving into their bonds allows us to block significant income for years to come.

Your retirement needs to be paid for, and buying low-risk investments like baby bonds can be a way to enjoy that income without the worries that a common dividend can’t match. BW’s ability to pay its current interest costs is not in question now, and its continued revenue growth makes being a bondholder attractive.

Looking at BWSN and BWNB, we would personally initiate a position in whichever has a better yield to maturity at the time of purchase, we provide real-time YTM data on our model portfolio for High Dividend Opportunities members to facilitate this for them.

Buy income, relax, get paid, repeat. That’s the beauty of income investing.