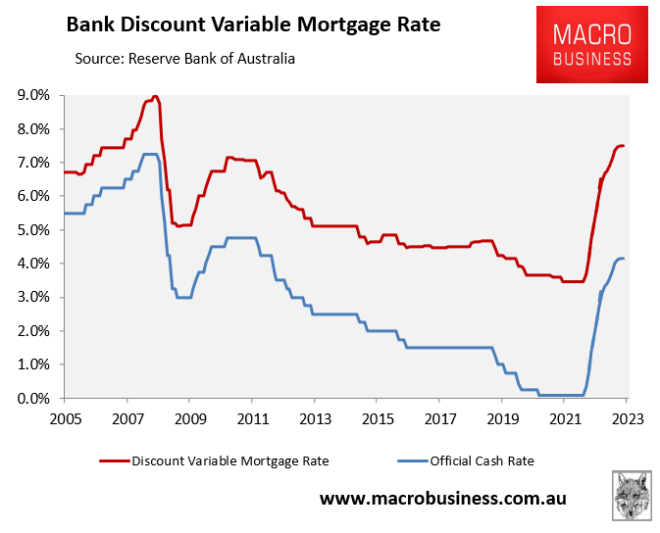

Just when you thought the Australian bond market couldn’t get any crazier about interest rates, on Friday it tipped the official Australian exchange rate (OCR) to peak at 4.15% in mid- 2013:

Fancy 4.0% interest rate hikes in just 12 months?

If the bond market forecast comes true, it would mean Australia’s OCR would rise by around 4.0% in just one year – by far the fastest increase in history.

It would also take Australia’s average discount variable mortgage rate to 7.50% by June 2023, well over double the 3.45% that prevailed just before the first interest rate hike in the UK. RBA in April 2022:

The bond market is pointing to the highest mortgage rate since October 2008.

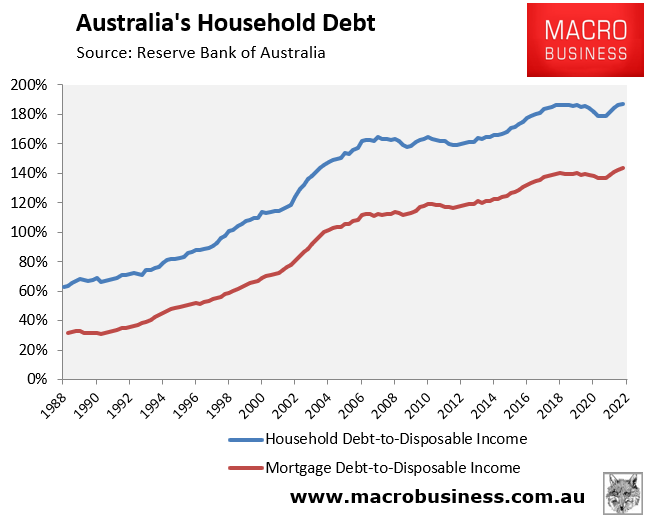

This would be the highest discount variable mortgage rate since October 2008 and comes at a time when household and mortgage debt in Australia has never been higher:

Australian household and mortgage debt has never been higher.

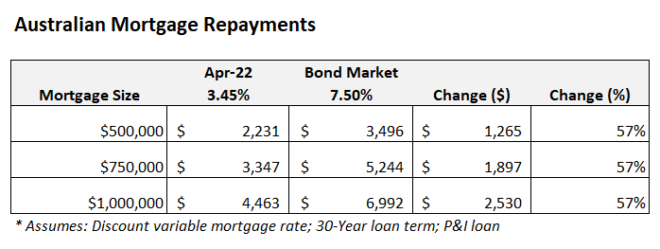

The impact on mortgage holders of the bond market OCR forecasts is shown in the table below. A household with an average discount variable mortgage would see their mortgage payments increase by 57% compared to their level before the April 2022 tightening:

Australian mortgage repayments would climb 57% according to bond market forecasts.

For a household with a $500,000 mortgage, this would represent a whopping $1,265 increase in monthly mortgage payments.

Thousands of Australian households would be forced into severe mortgage stress as property prices plummet.

The Australian economy would also be plunged into a deep recession as household consumption, the main driver of economic growth, would contract sharply, as households would have far less disposable income to spend.

For these reasons, we should all hope that the bond market gets it wrong and that the RBA doesn’t raise rates so aggressively.

Otherwise, households and the economy face Armageddon interest rates.

Leith van Onselen is Chief Economist at MB Fund and MB Super. He is also chief economist and co-founder of MacroBusiness.

Leith previously worked at Australian Treasury, Victorian Treasury and Goldman Sachs.