HarriesAD/E+ via Getty Images

Written by George Spritzer, co-produced by Alpha Gen Capital

Author’s note: This article was published for Yield Hunting members on September 20, 2022. Please check the latest data before investing.

The first Dynamic Europe Equity Trust Income Fund (NYSE: FDEU) is a diversified closed-end fund whose objective is to provide a high level of current income and some capital appreciation. It invests at least 80% of its managed assets in European equities of any market capitalization, including common and preferred stocks and REITs. The fund is currently selling covered call options against 32% of the portfolio.

(The data below comes from the First Trust fund website, unless otherwise stated.)

FDEU does not hedge its currency exposure, so by holding the fund you are gaining some exposure to the euro. By investing in an ETF like UUP (or a short FXE position), you can hedge some of this currency risk. But I like to keep it simple and not be hedged because I think the money side tends to balance out over the long run.

An interesting feature of the European stock market is the spread between the dividend yield of equities and that of 10-year government bonds. In Germany, the yield on 10-year government bonds is 1.76% and in France it is 2.30%.

SPDR Portfolio Europe ETF (SPEU), a broad based European ETF, has a dividend yield of 3.89%. The stock dividend yield spread is several hundred basis points. Compare that to broad-based US ETFs, where the stock dividend spread is negative or nearly flat. FDEU has a payout yield of 6.89% which has an even greater spread as it improves its yield via the writing of covered call options.

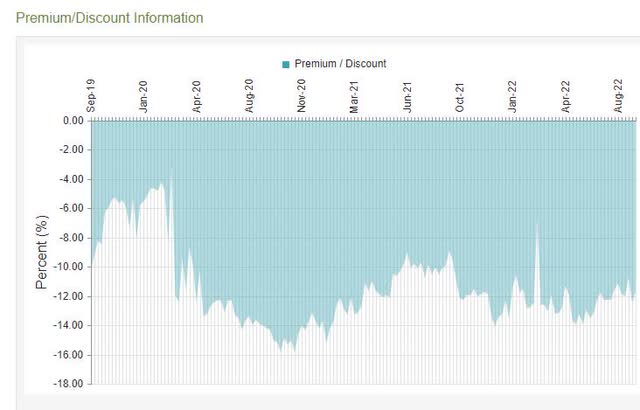

As of Monday’s close, FDEU was trading at a -11.85% discount to its net asset value. That’s close to its 52-week average discount of -12.23%. But the discount still looks quite steep due to the fund’s upcoming contingent conversion feature.

FDEU is a well-diversified fund with the top ten holdings accounting for approximately 27% of the portfolio. Here are the top ten holdings in the FDEU portfolio as of August 31, 2022 taken from the fund’s website:

Top 10 FDEU assets (as of 08/31/2022)

|

Nestlé SA – CHF |

3.43% |

|

Sanofi – EUR |

3.27% |

|

BHP Group Ltd. -GBP |

2.76% |

|

Imperial Brands PLC – GBP |

2.67% |

|

Roche Holding AG – CHF |

2.66% |

|

Novartis AG – CHF |

2.54% |

|

Astra Zeneca PLC – GBP |

2.52% |

|

Shell PLC – EUR |

2.47% |

|

Unilever PLC – EUR |

2.45% |

|

Total Energies SE- EUR |

2.40% |

The top 10 holdings are all strong global companies. The two main sectors of the fund are financials and healthcare. This is the breakdown of the top ten sectors as of August 31 on the fund’s website.

Breakdown by industrial sector (as of August 31, 2022)

|

finance |

17.01% |

|

Health care |

14.05% |

|

Basic consumption |

11.94% |

|

Consumer Discretionary |

11.28% |

|

Industrial |

11.17% |

|

Energy |

8.76% |

|

Communication Services |

7.25% |

|

Materials |

6.46% |

|

Utilities |

6.46% |

|

Computer science |

2.99% |

|

Immovable |

2.63% |

It should be noted that the weighting of the information technology sector is quite low at 2.99%.

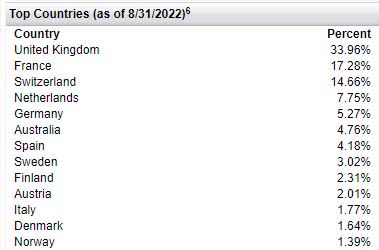

Breakdown by FDEU country (First Trust website)

The FDEU has a base annual expense ratio of 1.65%, which is quite high, but not unusual for CEFs that hold foreign equities. For equity CEFs, I like to see the discount of at least ten times the expense ratio. FDEU does not qualify using this standard. But the contingent conversion function helps overcome this.

FDEU three-year discount history

History of FDEU discounts (cefconnect)

FDEU Net Asset Value Performance History

Total return % FDEU (NAV) European Equity

|

5 years |

-2.73% |

-1.30% |

|

3 years |

-1.70% |

-0.32% |

|

1 year |

-15.16% |

-20.36% |

|

YTD |

-18.64% |

-22.45% |

|

3 months |

– 5.19% |

– 4.02% |

(Source: Morningstar)

Here are some other summary stats for FDEU:

First Trust Dynamic Europe Equity Income Fund (FDEU)

- Total assets: 277 million

- Joint assets: 205 million

- Creation date: September 24, 2015

- Create action price = $20.00

- Last Monthly Distribution = $0.06

- Annual distribution = $0.72

- Distribution yield = 6.86%

- Fund expense ratio: 1.65%

- Discount on NAV = -11.85%

- Average discount over 6 months = -12.38%

- Z-stat over 1 year for the rebate = +0.38

- Portfolio turnover rate: 33%

- Leverage: 26%

- 3-month average daily volume (stocks) = 47,000

- Average dollar volume = $490,000

Contingent conversion function

One of the main reasons I like FDEU here is its contingent conversion feature. When the fund first went commercial in 2015, this feature was often used by fund sponsors to help raise funds for the closed-end fund’s IPO.

The feature provides that in calendar year 2023, the Fund will call a meeting of shareholders for the purpose of voting on whether the Fund should convert to an open-end investment company. But the meeting may be adjourned or postponed in accordance with the Fund’s articles of association to a date in the calendar year 2024.

The conversion vote requires the approval of a majority of the Fund’s outstanding voting securities as defined by the 1940 Act. circulation” requires one of the following conditions:

- 67% or more of the shares present at a meeting, if the holders of more than 50% of the shares are present or represented by proxy. WHERE

- More than 50% of the shares, whichever is lower.

If shareholders approve, the Fund will seek to convert to an open-ended investment company within 12 months of such approval. If the number of votes required to convert the Fund into an open-ended investment company is not obtained on the Conversion Vote Date, the Fund will continue to operate as a closed-end investment company.

What are the odds of the Fund actually converting in 2024?

I think the management of the fund probably doesn’t want the fund to turn into an open-ended fund. They could lose a good chunk of their future stream of management fee income if enough investors decide to sell the open-end mutual fund at net asset value. For this reason, the conditional conversion feature is not promoted on the First Trust homepage or fund information sheet. If you haven’t read the prospectus carefully, you might not even know this feature existed.

Since many investors do not vote on shareholder proposals, it can be very difficult to obtain the majority of votes needed to convert to an open-ended fund. Two conditions are generally required:

-

The discount must be large enough to induce shareholders to vote in favor of the conversion.

-

A good portion of the shareholding should be made up of active investors who vote on shareholder proposals. Ownership by activist institutions or funds makes it easier to get the required vote, especially when the discount is large enough.

In the case of FDEU, I think the contingent conversion vote has a good chance of passing if the discount stays close to 10% next year. Institutional investors hold 62% of the outstanding shares. Here are the main shareholders as of June 30, 2022:

Name of shareholder Value in $ (MM)

|

Allspring Global Investments |

$39.7 |

|

City of London |

$17.8 |

|

1607 Capital Partners |

$13.9 |

|

SIT Investment Associates |

$9.1 |

|

Morgan Stanley |

$5.3 |

Some other activist investors such as Bulldog Investors currently have smaller positions in FDEU, but could very well add to their holdings in 2023 if the FDEU discount remains high. I also think the shareholder base may attract more active investors, who tend to vote, as more people learn about the contingent conversion feature of this fund.

FDEU is a reasonable buy here for a longer-term investor who is willing to hold the fund with a good chance that the discount will narrow in 2023. If the discount narrows enough, you’ll likely make a good profit. If the discount doesn’t drop below about 7%, I think there’s a good chance the fund will convert to an open-end mutual fund in 2024.

A reasonable alternative is the SPEU, which has a much lower expense ratio of 0.09%. But I still prefer FDEU, if you can buy it with 12% discount from full price for SPEU.