Flavio Vallenari/E+ via Getty Images

The iShares MSCI Switzerland Capped ETF (NYSEARCA:EWL) is a European ETF that focuses on some of the most well-known blue chip exposures. The Swiss element is totally irrelevant, and the only Swiss element that connects these stocks is that they all trade on Swiss stock exchanges, often among others. It’s a small ETF, so are the main stocks driving the portfolio all that good in the current environment? Not really. There’s nothing too compelling here with this ETF.

Distribution of the LEF

Let’s take a look at the main holdings.

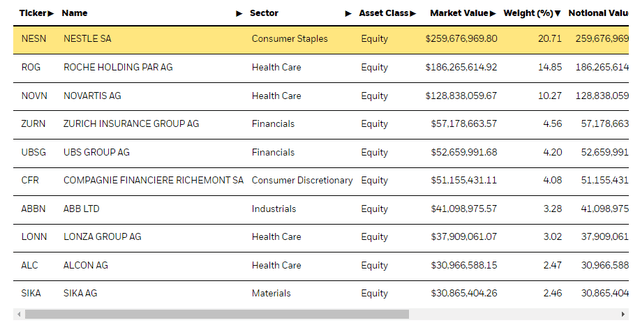

Main titles (iShares.com)

Large holdings start with Nestlé (OTCPK:NSRGY) at 21%. Nestlé is one of the largest consumer staples companies. Its share of portfolio is geographically very large, with the United States accounting for 30%, but the rest of the exposures are widely spread across the world. Beverages, pre-made foods, dairy products and consumer food products classified as nutritional products constitute the bulk of income. They also make pet food, where the number of pet owners has increased a lot since the pandemic – it has apparently more than doubled in the United States. These are pretty strong categories, but there is always downside risk with a stressed macroeconomic environment. Cash flow isn’t completely strong, but the company is valued at an earnings yield below risk-free rates. Too premium in our opinion and not interesting.

Roche (OTCQX:RHHBY) can’t even rely on premiumization from a rock-solid profile. They face competition from biosimilars and have a problem with a diagnostic revenue surge that is now collapsing as COVID-19 becomes increasingly irrelevant in the West. Novartis (NVS) is stronger and even trading cheaper than Roche despite a stronger outlook. Roche doesn’t look good, Novartis looks better, and together they make up 25% of the portfolio, where healthcare exposures together make up 33%. The rest of the healthcare exposures are likely strong, with Alcon (ALC) in eye care products and others looking decent.

Financials is the other major category led by Zurich Insurance (OTCQX: ZURVY). Insurance companies and financial companies are strong in that a higher rate environment benefits them considerably. Insurance companies are getting higher returns on investment portfolios and banking exposures are seeing higher net interest income. Insurance is the biggest presence in the financial exposure here, and that’s fine. Insurance companies have an attractive economy and cash flow generation in a period when liquidity is finally becoming a little scarcer.

conclusion

The ETF contains 47 stocks. It is little. And as is typical of small ETFs, it doesn’t run very cheap. An expense ratio of 0.5% is not ideal for the passive investor. Additionally, many of these stocks feature prominently on other European value-weighted ETFs, even the iShares Core MSCI Europe ETF (IEUR) has all of these stocks, albeit in smaller amounts. In this case, it’s for the best because the EWL elements aren’t that stunning. It’s not a risk-free portfolio, but the implied earnings yield of a 15x PE barely exceeds the risk-free rates. The only advantage for the European investor is that some of these companies’ cash flows are denominated in dollars, which has alleviated pressures on certain fundamentals. Nothing binding here.

While we don’t often do macro views, we do occasionally on our market service here on Seeking Alpha, The laboratory of value. We focus on long-term value ideas, where we try to find undervalued international stocks and target a portfolio return of around 4%. We’ve done very well over the past 5 years, but we had to get our hands dirty in the international markets. If you are a value-oriented investor concerned with protecting your wealth, we at the Value Lab could be a source of inspiration. Try our no-obligation free trial to see if it’s right for you.