Imaginima

With the latest developments around its iPhone 14 and its agreement with Globalstar (GSAT) for satellite communications completely independent of terrestrial cellular mobile networks, Apple (NASDAQ: AAPL) seems to lay the groundwork for a broader telecommunications role that is expected to significantly increase the number of devices sold in fiscal year 2023.

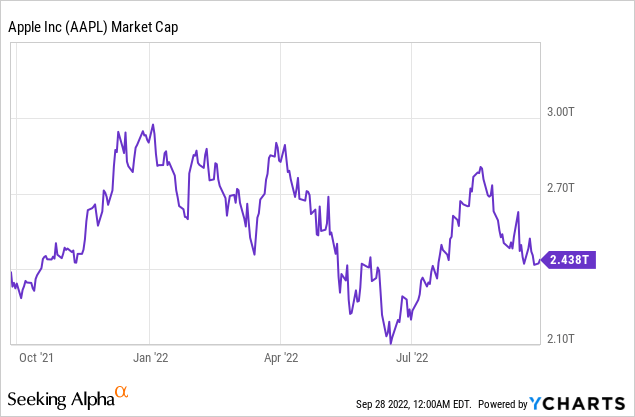

In doing so, it adds to the size of its market which is already worth trillions of dollars, while at $2.4 trillion its market capitalization is down 20% from its January 2022 peak of $3 trillion. of dollars.

In addition to determining a target share price in light of new opportunities, this thesis will examine competition, as well as how Apple’s decisions challenge years-old partnership agreements with service providers. mobiles.

Changes made by Apple

One of the major changes is Apple’s complete removal of the SIM card tray. This is where you insert the SIM module, which identifies you as a subscriber on a particular operator’s network. It went from the large SIM card of five years ago to the Nano SIM, until Apple effectively reduced its size to zero. This may seem like a small change, but represents a paradigm shift, as it implies that Apple now exclusively favors eSIM or electronic SIM card.

iPhone 14 (www.apple.com)

SIM card scanning is not a new concept as it is supported by previous iPhone models and is already offered by many carriers, but it is offered as an addition to existing physical cards, especially when you travel abroad. This saves the hassle of having to physically swap the SIM card at each destination, with eSIM-only even being considered a “more secure alternative to a physical SIM card”.

In this respect, such changes have already been tried by others before, notably Motorola (MSI), about 3 years ago, without much success. However, this time it is the turn of the giant Apple which claims more than 50% of the American smartphone market. The company is also adept at transformational changes such as removing the headphone jack from its iPhone 7, which was later followed by the industry’s move to wireless.

Still, it’s debatable whether Apple’s gamble might backfire on carriers that don’t provide its device as part of their plans, as the iPhone 14 makes it possible to have many cellular plans at the same time. time, which means that it is easier for subscribers to switch providers too. In the same vein, given the recent agreement with Globalstar for satellite communications in areas without cellular coverage, Apple appears to be laying the groundwork for a broader role in the telecom ecosystem.

With the stakes so high, it becomes important to assess what competitors are doing.

The competition

According to a source, Google (GOOG)(GOOGL), has started programming its Android 14 software to support direct satellite phone connectivity. Now, Google already has a longstanding partnership with T-Mobile (NASDAQ:TMUS) that dates back to 2008 for cellular and WiFi testing on the G1. Interestingly, earlier this month Google’s VP of Platform and Ecosystems talked about “designing for satellites.” Now, this announcement comes just a week after T-Mobile’s collaboration with SpaceX (SPACE) for satellite connectivity, as I covered in my thesis in August.

Google Collaboration with T-Mobile for Open Infrastructure Cloud (seekingalpha.com)

Now, in addition to the Android version which will not be available until mid-2023, the device, whether it is a Samsung (OTCPK:SSNLF) Galaxy, Xiaomi (OTCPK:XIACF) or Oppo, must all be equipped with the correct modem that can provide direct satellite access. Contrast that with Apple and Globalstar who have already conducted feasibility studies, including field testing, with the service scheduled to launch this very year. To support the launch, a satellite feature, which is most likely Qualcomm’s (QCOM) X65 modem including Globalstar’s 53 band already equips the latest iPhone 14s as I explained in a previous thesis.

Continuing further, Apple may face future competition from other companies like Samsung, in addition to AST SpaceMobile (ASTS), or Lynk Global which are in more advanced testing phases, but, the fact that it has better control of its smartphone ecosystem since it owns IOS software and iPhone hardware gives it more agility than competitor Google. Also, thanks to one of the most recognizable brands, Apple can aggressively drive the adoption of its satellite-direct iPhone and it should be priced accordingly.

The global satellite phone market is expected to reach $5.2 billion in 2027 from $3.8 billion in 2019, or grow at a CAGR of 4%. However, this includes traditional players like Iridium (IRDM), Globalstar and Thuraya etc. offer satellite phones (pictured below) with subscription plans averaging $835 per year, plus additional charges based on the number of voice calls made. Now, unless you’re a professional hunter, sailor, or ranger, these fees and the inconvenience of using a satellite phone in addition to your smartphone may deter you from subscribing to a cellular phone service. satellite. This is more of a niche market with millions of units considering that the total number of smartphones is expected to reach 7.33 billion in 2025 from 6.37 billion in 2021.

Image of a satellite phone (investors.globalstar.com)

Therefore, by commoditizing the satellite phone market, Apple should scale it well beyond the $5.2 billion mark, depending on how it drives its iPhone 14 in replacement of features such as SOS calls which are traditionally provided by specialized and relatively expensive devices. Now add to that the $6.3 trillion in existing opportunity from the app economy (apps for smartphones), which includes revenue from Apple’s services, namely advertising, and AppStore commissions , and it becomes clear that the company deserves to be widely valued.

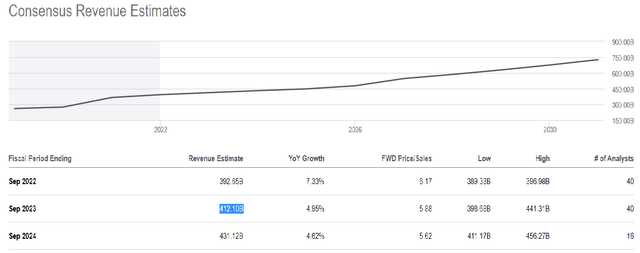

As for valuations, the company generated $190 billion from iPhones in 2021, or 52% of total revenue of $365 billion. It sold 13.5% more units in 2021 than in 2020, but little progress is expected for the 2022 fiscal year which ends in September. Assuming the growth rate doubles in fiscal year 2023 (October 2022 to September 2023) to 27% due to increased direct sales of iPhone 14 via satellite, this should translate to 51 $.3 billion (190 x 0.27) in device revenue. Adding that to the $412.1 billion in expected sales for 2023, I get $463.4 billion, or 12% more. Multiplying this by the forward price-to-sales ratio of 5.87x gives me a revised P/S of 6.6x for 2023. This translates to a stock price of $170.7 (151.8 x 1.12), based on the current stock price of $151.8, making Apple a buy.

Consensus revenue estimates (www.seekingalpha.com)

The $463.4 billion expected for 2023 does not include services that made up 18% of revenue in 2021. ’emergency’ via satellite and generate more sales in return. This feature will be available for an initial two-year period initially covering the US and Canada and can prove lifesaving for someone stranded in a remote location without mobile coverage or in the event of a fire or flood. These are strong enough reasons to believe that subscribers will be willing to upgrade their iPhone or Android users by making the switch.

On the other hand, Apple will have to pay Globalstar between 185 and 230 million dollars as part of the partnership agreement, while providing the service for free. Also, the removal of the SIM tray somehow calls into question partnership agreements with carriers, whereby carriers would sell iPhones as part of their 5G service plans, thereby indirectly subsidizing Nasdaq’s most valued company. .

Therefore, it’s important to watch how Verizon (VZ) and AT&T (T) adjust to Apple’s new role, especially since they already have partnerships with Google for private cloud and data networks. periphery. Additionally, with the Federal Reserve unlikely to turn dovish anytime soon, more value-oriented investors may choose to monitor next-year profitability before investing.

Conclusion

Still, with an A+ profitability rating, Apple’s margin is unlikely to be affected much, as the company may also adjust product prices to offset the additional costs. Also, it’s hard to imagine Verizon or AT&T being a hindrance, given that the satellite service is only for low-bandwidth messaging, not fifth-generation wireless, implying that Apple do not venture into their territory. On the contrary, they can sell more subscriptions.

Therefore, Apple’s foray into satellite communications is aimed at bolstering slow iPhone sales, while at the same time this ability to come up with a plan to increase market share through innovation is bold. and therefore I have a price target of $170.7.

To end on a note of warning, after the feasibility and testing phases, comes the implementation when subscribers actually start using the new satellite direct iPhone, which means that depending on how updates product adoption updates hit the market, stock can be volatile. .