Mauricio Graiki/iStock via Getty Images

A lifestyle hedged in US dollars

I never understood why babies insist to take off their socks and throw them out of the stroller when the parents aren’t looking. I had involuntarily trained myself to accepting baby socks as largely disposable items at the time my wife and I took a trip to France and found ourselves in need yet another spare pair of socks for our (again) barefoot baby. But I was completely appalled when I did the currency conversion and found that this nondescript pair of grocery store quality baby socks was over $30 in France!!! I thought “there’s no way we can ever afford to live in Europe with the US dollar trading at $1.30…what if the US dollar keeps falling!” And guess what? It made! A few years after the Great Sock Shock, the euro rose relentlessly from around $1.30 to a dizzying nosebleed level of almost $1.60 – which would have driven the price of those little socks up in cotton at $40 or more.

I never fully recovered from the Great Sock Shock. This scared me enough when we were considering moving to Portugal in 2015, I was very wary of currency fluctuations and the sobering impact they can have on an American expat’s budget. I’m always nervous about currency fluctuations, but after seven years of living in Portugal, this particular year caught my eye. The reason is that we got real life experience with what we never expected: living abroad can provide some accidental hedging against falling stock prices.

Our portfolio is down this year – probably like yours and most others’. We weight most of our portfolio towards US stocks that pay dividends in US dollars (which we use for all our spending needs here in Europe). Thanks to the surge in the US dollar (which is up 16% against the euro this year according to Google Finance), our purchasing power has increased significantly this year, even after taking into account the cost of l ‘inflation.

USD/Euro (Google Finance)

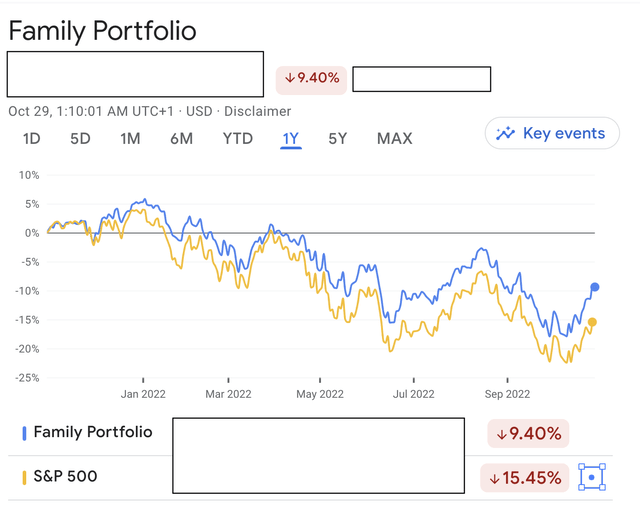

And what about our net worth (mostly) denominated in US dollars? Here’s a snapshot of our family portfolio over the past year, measured in US dollars. Ignoring reinvested dividends, Google Finance calculates our total one-year loss at -9.4% compared to a -15.45% loss for the S&P 500. Not much fun there.

USD Wallet (Google Finance)

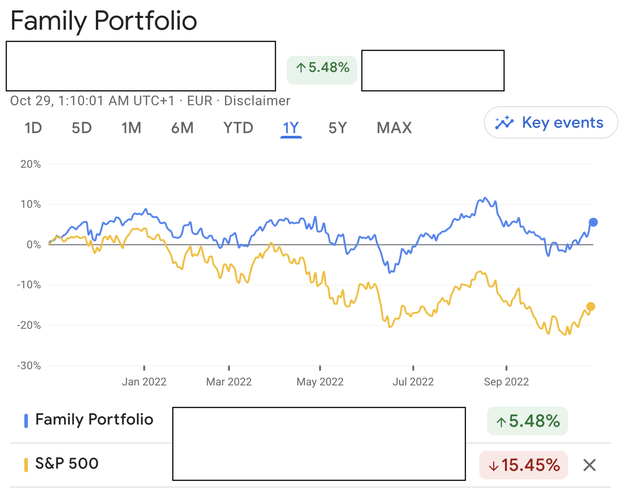

But since most of our spending is in euros, changing the denomination of our portfolio to euros better reflects changes in our real economic situation over the past year. Measured in euros, our portfolio is actually up 5.48% over the past year according to Google Finance – thanks to the soaring US dollar. So even after suffering a very unwelcome stock market crash, the bear market has not undermined our ability to spend.

Euro wallet (Google Finance)

So, was the accidental 2021 hedge some kind of fluke? To find out, I downloaded all closing prices for the US dollar against the euro from December 2003 and all closing prices for the S&P 500 Index ETF (SPY) over the same period (both sets of data I found on Yahoo Finance). Then I calculated the statistical correlation between the two sets of data and learned that there was a moderate inverse correlation of around -0.58 between the US dollar against the euro and the S&P 500 (you can access the calculations here). This means that if you own US stocks and live in Europe, history shows that the gains on your stock portfolio are somewhat likely to cushion the blow to your purchasing power when the US dollar falls against the euro. Conversely, when your US equity portfolio falls, it is somewhat likely that the US dollar will be higher and will likely offset some of your losses in purchasing power. So it turns out that 2021 was no coincidence at all, and living abroad box be a moderate hedge against falling stock prices…just like rising stock prices box be a hedge against the fall of the US dollar. In this sense, perhaps you can consider living abroad as a kind of “lifestyle hedge”.

Investing for cash flow in US dollars.

I would argue that the main challenge of owning US assets while living overseas comes down to building a portfolio that pays steady and growing dividends paid in US dollars. This way, when the US dollar is strong, your Euro living expenses will tend to be lower, making it easier for you to save money that you can reinvest. From stock prices tender tracking down when the US dollar is strong means you’re more likely to get good deals every time you reinvest. Conversely, if the US dollar is weaker, you will find that your daily spending in euros will increase. From stock prices tender to rise when the US dollar is lower, you’ll likely find that you have a bigger cushion of capital in case you need to sell stocks to supplement your dividend income to keep pace with those euro expenses growing. Anyway, my personal experience is that investing in dividend growth can work especially well if you’re an American living overseas.

And it’s surprisingly simple to build a portfolio of ETFs that offer a relatively steady and growing stream of dividends paid in US dollars; you could hold the Schwab US Dividend Equity ETF (SCHD) which yields 3.37%, the Vanguard Dividend Appreciation ETF (VIG) which yields 1.99%, the Proshares S&P 500 Dividend Aristocrats ETF (NOBL) which yields 2.06% . Or there’s my approach: create your own dividend growth ETF by buying (and then passively holding) a representative sample of individual stocks that funds such as (SCHD), (VIG) or (NOBL) might hold. I chose this approach because I have several investment criteria that no dividend growth ETF explicitly follows. First, I insist on owning nothing but companies with little or no debt. When interest rates rise, highly leveraged companies face higher interest charges that eat up a larger share of earnings and reduce the ability to pay dividends. This is why about 90% of the capital in my portfolio is concentrated in companies with no debt or with a credit rating of A or better. I will not own any business with a credit rating below investment grade. SecondI only own companies with very high profit margins and sustainable dividend payout ratios. Third, I only want to own businesses with locked-in revenue streams (such as long-term contract revenue, large business moats such as unrepeatable train lines, or proven, unwavering brand loyalty). Low-risk dividends from low-risk companies increase the likelihood of actually receiving the dividends you expected. Because let’s never overlook the most important thing about income: put it in your hands in full and on time.

Here is our current portfolio. The majority of our income is in the form of US dollars, but we also own non-US stocks which pay dividends denominated in Swiss Francs, Canadian Dollars, British Pounds and Euros (although we receive actual distributions in US dollars depending on the exchange rate then in effect). For this reason, our portfolio is not a perfect “US dollar lifestyle hedge”, but when it comes to creating a DIY stock index based on quality and income security, I think the functional currency of the business is much less important than the quality of the business. products and services.

Author Portfolio (authors spreadsheet, returns from SeekingAlpha.com)

Which brings me back to the notorious case of the $30 French socks from the grocery store. We ended up choosing to affix these socks to the baby’s pants using two diaper pins (which only eased the shock of my sticker somewhat). And the days of weekly restocking of baby socks are now well over, leaving us with all the other great reasons to enjoy life in Portugal:

(1) Brilliant Lisbon Sunsets (with our former baby now towering over her mother);

Sunset in Bairro Alto (Photo by the author)

(2) gorgeous tiles and architecture;

Old wine and tobacco store in Cascais (Photo by the author)

(3) thunderstorms on the beach with a thermos of hot coffee; and

Guincho beach as a storm approaches (Photo by the author)

4) Aged sheep cheese and white wine with mercado.

Mercado cheese and wine stand (photo by the author)